The pending administration decision on whether to impose a tariff or other fee on US imports of solar equipment from China raises serious concerns. The right choice in this case is less obvious than suggested by the jobs and free-trade arguments from the main US solar trade association (SEIA) or the Wall St. Journal's editorial page. Solar power generates less than 2% of US electricity today. However, if it is to grow as experts forecast and advocates claim is essential, then considerations such as long-term energy security can't be ignored, while near-term job losses from a new tariff would be more than offset by subsequent growth.

Last October the US International Trade Commission issued its recommendations in favor of the complaint by two US manufacturers of solar panel components. I usually favor low tariffs and open access, especially when the markets in question are functioning smoothly and the principal impacts from trade are the result of "comparative advantage" in production or extraction between countries. However, there is little about the market for solar equipment, including the photovoltaic (PV) cells and modules at issue here, that qualifies as free.

The production and deployment of solar energy hardware has depended since its inception, and from one end of its value chain to the other, on significant government interventions. In the case of China-based PV manufacturing, these have included low-interest government loans, preferential access to land, and minimal environmental regulations. China-based PV manufacturers were also able to take advantage of extravagantly generous European solar subsidies in the 2000s to scale up their output, drive down their costs, and ultimately send much of the EU's solar manufacturing industry into bankruptcy.

On the US end, both solar manufacturing and deployment (installation) have benefited greatly from federal tax credits, cash grants from the US Treasury, and a web of state quotas for aggressively increasing utilization of renewable energy sources. Justified on grounds of energy security, "green jobs", and climate change mitigation, these measures have strongly promoted solar power and delivered an extraordinary 68% compound annual growth rate in US solar installations since 2006. On a per-unit-of-energy basis, these supports are also at least an order of magnitude more valuable to the solar industry than the federal tax benefits received by the oil and gas industry.

One of the factors that makes this decision so difficult and politically sensitive is that a whole industry has apparently grown up around cheap solar imports, to the point that the main solar benefit to the US economy today is from installation, not manufacturing. US companies and their employees build solar panel racks and other "balance of system" gear, finance rooftop and other solar projects, and construct these installations.

These companies could be at risk of losing business and shedding jobs, if a large tariff were imposed on imported solar cells, modules and panels. Those impacts might be less than feared, though, because the cost of the actual sunlight-converting PV hardware now makes up less than a third of total solar project costs. In other words, a tariff that doubled effective PV cost would drive up total solar costs to a much smaller degree, and least of all for residential solar, which has the highest total costs per kilowatt.

There's another important aspect of this debate that hasn't received much attention. If solar power is as important to our future energy diet as many think, then it should be no more desirable to become heavily reliant on China for our supplies of PV components than it did to depend on growing imports of Middle East oil. That was the main energy security issue for the US for the last 30 years, until the shale revolution unexpectedly reversed that trend. Relying on solar imports from China in the long run will be nothing like depending on Canada for the largest share of the petroleum the US still imports.

It also makes sense to address this situation now, before solar power has grown to 20% or 30% of the US electricity mix, and with the US economy near full employment, when those workers that did lose their jobs would have the best chance to replace them quickly.

From the start, the complaint of unfair competition lodged by Suniva Inc. and Solar World Americas--Chinese- and German-owned, respectively--has been derided as an effort to prop up a couple of marginal players at the expense of the much larger US solar-installation sector. That ignores the position of First Solar (NASDAQ:FSLR), a US-based PV manufacturer with $3 billion in global sales. The company is on record supporting the trade complaint. Of course they aren't a disinterested party; they stand to benefit from a tariff that would raise the cost of competing PV gear from China and elsewhere.

That's precisely the point of the complaint: strengthening US solar manufacturers, so that the growth of solar energy in this country doesn't end up like TV sets and other consumer electronics. There's more at stake, because PV isn't TV. If solar power becomes a major part of US energy supplies by mid-century, it will actually matter if we have a robust manufacturing base to drive its deployment, rather than relying on any one country or region for its key building block.

Showing posts with label energy security. Show all posts

Showing posts with label energy security. Show all posts

Friday, January 19, 2018

Wednesday, August 06, 2014

The Missing Oil Crisis of 2014

- While the full impact of the surge in US "tight oil" may be masked by problems elsewhere, it is on the same scale--but opposite direction--as key factors that led to the 2007-8 oil price spike.

- In that light it does not seem like hyperbole to credit the recent revival of US oil output with averting another global oil crisis.

Although shale energy development certainly deserves to be called revolutionary, crediting it with averting an oil crisis calls for a bit of "show me." Yet with problems in Libya, Nigeria and Iraq, while Iranian oil remains under sanctions and oil demand picks up again, even at first glance Mr. Yergin's assertion looks like more than a casual, lunch-speech sound-bite.

Start with current US tight oil (LTO) production of over 3 million barrels per day (MBD) and estimates of future LTO production rising to as much as 8 MBD--also the subject of much discussion at the conference. As recently as 2008 total US crude oil output had fallen to just 5 MBD and was only expected to recover to around 6 MBD by 2014, with minimal contribution from unconventional oil. Instead, the US is on track to beat 2013's 22-year record of 7.4 MBD, perhaps by as much as another million bbl/day.

With conventional production in Alaska and California declining or at best flat, and with Gulf of Mexico output just starting to recover from the post-Deepwater Horizon drilling moratorium and subsequent "permitorium", the net increase in US crude production attributable to LTO today is in the range of 2.5-3.5 MBD and growing, thanks to soaring output in North Dakota, Texas and other states.

That might not sound like much in a global oil market of over 90 MBD, but it brackets the IEA's latest estimate of OPEC's effective unused production capacity of 3.3 MBD. Spare capacity and changes in inventory are key measures of how much slack the oil market has at any time. When OPEC spare capacity fell below 2 MBD in 2007-8, oil prices rose sharply from around $70 per barrel to their all-time nominal high of $145 per barrel. It took a global recession and financial crisis to extinguish that price spike, and high oil prices were likely a major contributor to the recession.

Global oil inventories are now a little below their seasonal average for this time of the year. Compensating for the absence of over 3 MBD of US tight oil would require higher production elsewhere, lower demand, or a drain on those inventories that would by itself push prices steadily higher.

Concerning production, if the US tight oil boom hadn't happened, more investment might have flowed to other exploration and production opportunities. However, for non-LTO production to have grown by an extra 3 MBD, companies would have had to invest--starting in the middle of the last decade--in the projects necessary to deliver that oil now. Were that many deepwater and conventional onshore projects deferred or canceled because companies anticipated today's level of LTO production more than 5 years ago? And would Iraq, Libya and Nigeria be more reliable suppliers today if US companies hadn't been drilling thousands of wells in shale formations for the last several years? Both propositions seem doubtful.

As for adjustments in demand, US petroleum consumption is already over 8% less than in 2007. And as we learned in the run-up to 2008, much of the oil demand in the developing world, where it has grown fastest, is less sensitive to changes in oil prices than demand in developed countries, due to high levels of consumer petroleum subsidies in the former. Petroleum product prices in the latter must increase significantly in order to get consumers there to cut their usage by enough to balance tight global supplies. That dynamic played an important role in oil prices coming very close to $150 per barrel six years ago, when average retail unleaded regular in the US peaked at $4.11 per gallon, equivalent to nearly $4.50 per gallon today.

So to summarize, if the US tight oil boom hadn't happened, it's unlikely that other non-OPEC production would have increased by a similar amount in the meantime, or that OPEC would have the capability or inclination to make up the resulting shortfall versus current demand out of its spare capacity. Demand would have had to adjust lower, and that only happens when oil and product prices rise significantly. With oil already at $100 per barrel, it's not hard to imagine such a scenario adding at least $40 to oil prices--just over half the 2007-8 spike. Combined with higher net oil imports, that would have expanded this year's US trade deficit by around $230 billion. US gasoline prices today would average near $4.60 per gallon, instead of $3.54, taking an extra $140 billion a year out of consumers' pockets.

We can never be certain about what would have happened without the current surge in US tight oil, but for a reminder of how a similar situation was characterized just a few years ago, please Google "2008 oil crisis". If we found ourselves in similar circumstances today, then the heated Congressional hearings and angry consumers to which Mr. Yergin alluded in his remarks would almost certainly have been major topics at EIA's 2014 conference, instead of the realistic prospect of legalized US oil exports.

A different version of this posting was previously published on the website of Pacific Energy Development Corporation.

Friday, March 28, 2014

How Can US Natural Gas Reduce Europe's Dependence on Russia?

- The EU's dependence on Russian natural gas is directly linked to its own gas production, which has fallen faster than EU member countries' demand for gas.

- While US LNG exports aren't an immediate remedy, due to permitting and construction time lags, the prospect of their availability is already affecting the gas market.

The European Union is expected to import 15.5 billion cubic feet (BCF) per day of natural gas from Russia this year, roughly half of which would normally be transported by pipelines passing through Ukraine. Worries about the security of these supplies in the current crisis are compounded by Europe's increasing reliance on gas imports from all sources.

While EU gas consumption, based on the union's 28 current member countries, has been essentially flat over the last decade, its production has declined by more than a third, as shown in the chart below. As of the end of 2012, EU self-sufficiency in gas stood at just 35%. The widening of the gap between EU gas demand and production bears a close resemblance to the situation in which the US found itself with regard to crude oil prior to the shale revolution, and it is the main source of Europe's vulnerability in natural gas.

_in_thousand_terajoules_(GCV)-tb1.png&filetimestamp=20130625095947){kind=link}

|

After Russia, the EU's main gas suppliers are Norway and Algeria, primarily by pipeline, followed by LNG sourced from Qatar, Nigeria and other countries. Russia's leading role in supplying Europe's gas is consistent with its status as the world's second-largest gas producer and largest gas exporter, its proximity to the EU, and its pipeline network developed over multiple decades. Europe's gas supply mix includes ample political risk, but none of the EU's other suppliers are geopolitical rivals like Russia.

The EU has three main options for reducing its dependence on gas imports from Russia. It could shrink natural gas consumption, which is already happening to a modest degree as pricey gas-fired power generation is being squeezed out between subsidized wind and solar power and cheaper coal power, in a mirror image of US trends of the last several years. This seems inconsistent with the EU's long-term emission goals and its need for gas to back up intermittent renewable electricity generation, so the further scope for this option appears limited, at least for the next decade.

EU countries could also attempt to revive domestic gas production. Europe's conventional gas fields may be in decline, other than in non-EU Norway, but its shale gas potential was estimated at 470 trillion cubic feet (TCF) in the US Energy Information Administration's global shale assessment last year. That's about 40% bigger than Europe's reserves and technically recoverable resources of conventional gas. Uncertainties on this estimate are still large, but it's in the same ballpark with the Marcellus shale in the eastern US, which currently produces over 14 BCF/day.

Unfortunately, initial efforts in Poland's shale have been disappointing, while Germany, France, and other countries have imposed explicit or implicit moratoria on shale gas development. Unless these policies are reversed in the aftermath of the Ukraine crisis, the EU will be unable to grow its way out of its dependence on Russia.

That leaves import diversification as the likeliest path for weaning Europe off Russian gas. This process is underway incrementally, hastened by previous Russian gas brinksmanship. Interest in US gas is understandable on many levels, not least because even after increasing production by around 17 BCF/day since 2006, US shale resources are expected to add another 13 BCF/day by 2020.

Energy experts have been quick to point out that the first US LNG exports won't be available for at least several years, and that companies, rather than governments, are the main parties involved in gas contracts. Customers in Europe will have to compete for US and other LNG supplies with customers elsewhere, especially in Asia, where China's gas demand is growing and Japan's post-Fukushima nuclear shutdowns have dramatically increased LNG imports.

These constraints are real. However, they ignore the ways in which changing the market's expectations about future LNG supplies--and potentially prices--could affect the calculations of Europe's gas buyers today and limit the political leverage that Russia's dominant gas export position conveys. Anecdotal reports suggest that US LNG is already a factor in contract renegotiations in Eastern Europe. As Amy Myers Jaffe of UC Davis and formerly the Baker Institute tweeted a few weeks ago, "it isn't about physical LNG cargo to Europe; it is about US exports promoting market liberalization (and) greater liquidity."

{kind=link}

The EU has three main options for reducing its dependence on gas imports from Russia. It could shrink natural gas consumption, which is already happening to a modest degree as pricey gas-fired power generation is being squeezed out between subsidized wind and solar power and cheaper coal power, in a mirror image of US trends of the last several years. This seems inconsistent with the EU's long-term emission goals and its need for gas to back up intermittent renewable electricity generation, so the further scope for this option appears limited, at least for the next decade.

EU countries could also attempt to revive domestic gas production. Europe's conventional gas fields may be in decline, other than in non-EU Norway, but its shale gas potential was estimated at 470 trillion cubic feet (TCF) in the US Energy Information Administration's global shale assessment last year. That's about 40% bigger than Europe's reserves and technically recoverable resources of conventional gas. Uncertainties on this estimate are still large, but it's in the same ballpark with the Marcellus shale in the eastern US, which currently produces over 14 BCF/day.

Unfortunately, initial efforts in Poland's shale have been disappointing, while Germany, France, and other countries have imposed explicit or implicit moratoria on shale gas development. Unless these policies are reversed in the aftermath of the Ukraine crisis, the EU will be unable to grow its way out of its dependence on Russia.

That leaves import diversification as the likeliest path for weaning Europe off Russian gas. This process is underway incrementally, hastened by previous Russian gas brinksmanship. Interest in US gas is understandable on many levels, not least because even after increasing production by around 17 BCF/day since 2006, US shale resources are expected to add another 13 BCF/day by 2020.

Energy experts have been quick to point out that the first US LNG exports won't be available for at least several years, and that companies, rather than governments, are the main parties involved in gas contracts. Customers in Europe will have to compete for US and other LNG supplies with customers elsewhere, especially in Asia, where China's gas demand is growing and Japan's post-Fukushima nuclear shutdowns have dramatically increased LNG imports.

These constraints are real. However, they ignore the ways in which changing the market's expectations about future LNG supplies--and potentially prices--could affect the calculations of Europe's gas buyers today and limit the political leverage that Russia's dominant gas export position conveys. Anecdotal reports suggest that US LNG is already a factor in contract renegotiations in Eastern Europe. As Amy Myers Jaffe of UC Davis and formerly the Baker Institute tweeted a few weeks ago, "it isn't about physical LNG cargo to Europe; it is about US exports promoting market liberalization (and) greater liquidity."

A decision by the US government to streamline the permitting and development of LNG facilities wouldn't enable US exports to displace Russian gas in Europe this year or next, but it would put Russia on notice that in the future it must compete in a market in which gas customers in Europe and elsewhere will have much greater choice. That would certainly complicate President Putin's plans.

A different version of this posting was previously published on the website of Pacific Energy Development Corporation.

Wednesday, March 19, 2014

Making Oil-by-Rail Safer

- A series of rail accidents involving trains carrying crude oil has focused attention on safety procedures and even the tank cars used in this service.

- Another concern is the variable characteristics of the "light tight oil "now shipped by rail in large quantities. That isn't the result of "fracking", but of the oil's inherent chemistry.

In the immediate aftermath of Lac-Megantic, the Federal Railroad Administration issued an emergency order on procedures railroads must follow when transporting flammable and other hazardous materials. And on February 21, 2014 railroads reached a voluntary agreement with the US Department of Transportation (DOT) on additional steps, including reduced speed limits for oil trains passing through cities, increased track inspection, and upgraded response plans. These steps have the highest priority, because crude oil loaded in tank cars doesn't cause rail accidents. Every incident I've seen reported in the last year began with a derailment or similar event.

At the same time, the packaging and characteristics of the oil can affect the severity of an accident. Investigators have focused on two specific issues in this regard, starting with the structural integrity of the tank cars carrying the oil. The vast majority of tank cars in this service are designated as DOT-111--essentially unpressurized and normally non-insulated cylinders on wheels. These cars routinely carry a variety of cargoes aside from crude oil, including gasoline and other petroleum products, ethanol, caustic soda, sulfuric acid, hydrogen peroxide, and other chemicals and petrochemicals.

Their basic design goes back decades, and even the older DOT-111s incorporate learnings from earlier accidents. A growing proportion of the US fleet of around 37,000 DOT-111 tank cars in oil service consists of post-2011, upgraded cars that have been strengthened to resist punctures, but the majority is still made up of older, unreinforced models. The Pipeline and Hazardous Materials Safety Administration (PHMSA) is studying whether to make upgrades mandatory, but some railroads and shippers aren't waiting. Last month Burlington Northern Santa Fe Railway, owned by Warren Buffet's Berkshire Hathaway, announced it would buy up to 5,000 new, more accident-resistant tank cars.

Another issue that has received much attention since Lac-Megantic concerns the flammability of the light crude from shale formations like North Dakota's Bakken crude, which accounts for over 700,000 barrels per day of US crude-by-rail. The Wall Street Journal published the results of its own investigation, reporting that Bakken crude had a higher vapor pressure--a measure of volatility and an indicator of flammability--than many other common crude oil types.

The Journal apparently based its findings on crude oil assay test data assembled by the Capline Pipeline. Although a Reid Vapor Pressure of over 8 pounds per square inch (psi) for Bakken crude is higher than for typical US crudes, it's not unusual for oil as light as this. That's especially true where, due to lack of field infrastructure, only the co-produced natural gas is separated out, leaving all liquids in the crude oil stream.

What makes this situation unfamiliar in the US is that domestic production of oil as light as Bakken had nearly disappeared before the techniques of precision horizontal drilling and hydraulic fracturing were applied to the Bakken shale and similar "source rock" deposits. (Note: High vapor pressures are characteristic of the naturally-occurring mix of hydrocarbons in very light crudes, rather than a result of the "fracking" process.) Nor is the reported vapor pressure for Bakken or Eagle Ford crude higher than that of gasoline, a product that is federally certified for transportation in the same DOT-111 tank cars that carry crude oil.

The variability of the vapor pressure data that the Journal's reporters identified for Bakken crude may result from another unfamiliar feature of such "light tight oil". Crude produced from conventional reservoirs, which are much more porous than the Bakken shale, tends to be relatively homogeneous. However, because the Bakken and other shales are so much less porous, limiting diffusion within the source rock reservoir, the composition of their liquids can vary much more between wells.

In any case, vapor pressure isn't the preferred measure of fuel flammability. Actual rail cargo classifications are based on flash point and initial boiling point. These routine quality tests aren't included in Capline's publicly available data. PHMSA initiated "Operation Classification" to ensure that manifests and tank car placards for crude oil shipments accurately reflect the potential hazards of each cargo, based on such measurements. The agency has determined that it hasn't always been done consistently, and DOT issued another emergency order requiring shippers to test oil for proper classification.

As mentioned in an oil-by-rail webinar yesterday, hosted by Argus Media, assigning the proper classification to oil shipments may seem like a bureaucratic concern--it doesn't necessarily affect the tank car type chosen to transport the crude--but it can have a significant impact on operational factors such as routing and the notification of first responders along the route.

There's no quick and simple way to make the transportation of crude oil by rail as safe as hauling a dry bulk cargo like grain. Tank car fleets can't be replaced overnight, not just because of the cost involved, but due to limited manufacturing capacity. However, in the meantime significant improvements can be achieved through a combination of government attention and sustained industry initiatives. Since the new crude streams traveling by rail play a key role in increasing North America's energy security, this is in the interest of everyone involved--producers, shippers, railroads, and not least the communities through which this oil travels.

{kind=link}

A different version of this posting was previously published on the website of Pacific Energy Development Corporation.

Tuesday, January 28, 2014

The Pros and Cons of Exporting US Crude Oil

- Calls for an end to the effective ban on exporting most crude oil produced in the US are based on a growing imbalance in domestic crude quality.

- At least recently, the ban has likely benefited refiners more than consumers. Assessing the impact of its repeal on energy security requires further study.

This isn't just a matter of politics, or of self-interest on the part of those benefiting from the current rules. Questions of economics and energy security must also be considered. The main reason these restrictions are still in place is that for much of the last three decades US oil production was declining. The main challenges for the US oil industry were slowing that decline while ensuring that US refineries were equipped to receive and process the increasingly heavy and "sour" (high sulfur) crudes available in the global market. The shale revolution has sharply reversed these trends in just a few years.

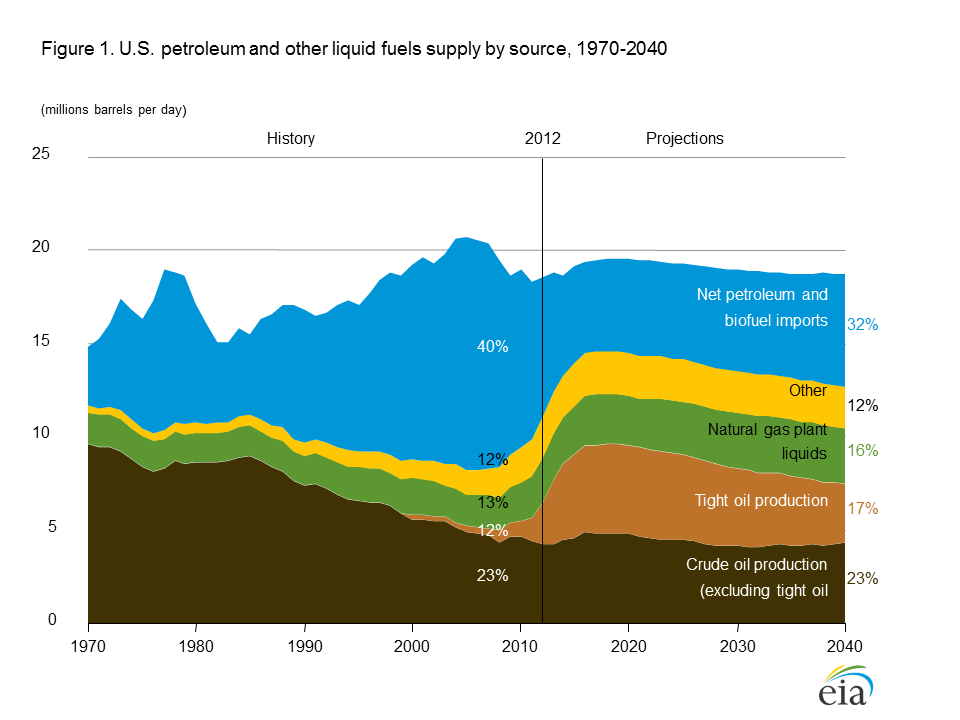

No one would suggest that the US has more oil than it needs. Despite the recent revival of production, the US still imported around 48% of its net crude oil requirements last year. Even when production reaches its previous high of 9.6 million barrels per day (MBD) as the Energy Information Agency now projects to occur by 2017, the country is still expected to import a net 38% of refinery inputs, or 25% of total liquid fuel supply. The US is a long way from becoming a net oil exporter.

The driving force behind the current interest in exporting US crude oil is quality, not quantity, coupled with logistics. If the shale deposits of North Dakota and Texas yielded oil of similar quality to what most US refineries have been configured to process optimally, exports would be unnecessary; US refiners would be willing to pay as much for the new production as any non-US buyer might. Instead, the new production is mainly what Senator Murkowski's report refers to as "LTO"--light tight oil. It's too good for the hardware in many US refineries to handle in large quantities, and for most that can process it, its better yield of transportation fuels doesn't justify as large a price premium as for international refineries with less complex equipment.

As a result, and with exports to most non-US destinations other than Canada or a few special exceptions effectively barred, US producers of LTO must discount it to sell it to domestic refiners. Based on recent oil prices and market differentials, producers might be able to earn as much as $5-10 per barrel more by exporting it. Meanwhile the refiners currently processing this oil are enjoying something of a buyer's market and are able to expand their margins. The export issue thus pits shale oil producers and large, integrated companies (those with both production and refining) such as ExxonMobil against independent refiners like Valero.

Producers are justified in claiming that these regulations penalize them and threaten their growth as available domestic refining capacity for LTO becomes saturated. Additional production is forced to compete mainly with other LTO production, rather than with imports and OPEC.

I believe producers are also largely correct that claims that crude exports would raise US refined product prices are mistaken. The US markets for gasoline, diesel fuel, jet fuel and other refined petroleum products have long been linked to global markets, with prices especially near the coasts generally moving in sync with global product prices, plus or minus freight costs. I participated in that trade myself in the 1980s and '90s. What's at stake here isn't so much pump prices for consumers as US refinery margins and utilization rates.

Petroleum product exports have become a major factor in US refining profitability, and refiners are reportedly investing and reconfiguring to enhance their export capabilities. This provides a hedge against tepid domestic demand. Nationally, refined products have become the largest US export sector and contributed to shrinking the US trade deficit to its lowest level in four years. If prices for light tight oil rose to world levels US refineries might be unable to sustain their current export pace. It's up to policymakers to assess whether that risk is merely of concern to the shareholders of refining companies or a potential threat to US GDP and employment.

The quest to capture the "value added"--the difference between the value of manufactured products and raw materials--from petroleum production is not new. It helped motivate the creation of the integrated US oil companies more than a century ago and impelled national oil companies such as Saudi Aramco, Kuwait Petroleum Company, and Venezuela's PdVSA to purchase or buy into refineries in Europe, North America and Asia in the 1980s and '90s.

On the whole, OPEC's producers probably would have been better off investing in T-bills or the stock market, because the return on capital employed in refining has frequently averaged at or below the cost of capital over the last several decades. It's no accident most of the major oil companies have reduced their exposure to this sector. When today's US refiners argue that it is in the national interest to preserve the advantage that discounted LTO gives them they are swimming against the tide of oil industry history.

The energy security case for crude exports looks harder to make. An excellent article from the Associated Press quoted Michael Levi of the Council on Foreign Relations as saying, "It runs against the conventional wisdom about what oil security means. Something seems upside-down when we say energy security means producing oil and sending it somewhere else." The argument hinges on whether allowing US crude exports would simultaneously promote more production and increase the pressure on global oil prices. That makes sense to me as a former crude oil and refined products trader, but it will be a harder sell to Senators, Members of Congress, and their constituencies back home.

The politics of exports may be easing somewhat, though, as a Senate vacancy in Montana could lead to a new Chair at Energy & Natural Resources who would be a natural partner for Senator Murkowski on this issue. (That shift may incidentally be part of a strategy to help Democrats retain control of the Senate.) Will that be enough to overcome election-year inertia and the populist arguments arrayed against it?

As for logistics, the administration could ease the pressure on producers without opening the export floodgates by exempting the oil output from the Bakken, Eagle Ford and other shale deposits from the Jones Act requirement to use only US-flag tankers between US ports. That could open up new domestic markets for today's light tight oil, while allowing Congress the time necessary to debate the complex and thorny export question.

Senator Murkowski wasn't alone in calling for an end to the oil export ban. In his annual State of American Energy speech presented the day as the Senator's remarks, Jack Gerard, CEO of the American Petroleum Institute, noted, "We should consider and review quickly the role of crude exports along with LNG exports and finished products exports, because of the advantages it creates for this country and job creation and in our balance of payments." In a similar address on Wednesday, the head of the US Chamber of Commerce stated, "I want to lift the ban. It's not going to happen overnight, but it's going to happen." I'd wager he at least has the timing right.

A different version of this posting was previously published on the website of Pacific Energy Development Corporation.

Thursday, November 07, 2013

Energy Security Four Decades After the Arab Oil Embargo

- The Arab Oil Embargo of 1973-74 focused our attention on energy security and set in motion drastic changes in the way we produce, trade and consume energy.

- With US energy output approaching or exceeding 1970s levels, some experts now advocate prioritizing competition from non-petroleum fuels over reducing oil imports.

The other, related purpose of the meeting was a presentation and discussion on the proposition that fuel competition provides a surer means of achieving energy security than our pursuit of energy independence for the next four decades following the Arab Oil Embargo. This idea warrants serious consideration, since energy independence, at least in the sense of no net imports from outside North America, is finally beginning to appear achievable.

The 1973-74 embargo was the first oil shock of a tumultuous decade, and it triggered a true crisis. The US had relied on oil costing around $3 per barrel (bbl), not just to fuel our transportation system, but also for 17% of our electricity generation and numerous other uses. The US was then one of the world’s largest oil producers but required imports comprising about one-third of supply to balance our growing demand. With the sudden loss of over a million barrels per day of oil imports from the Middle East, and lacking the sort of strategic petroleum reserve that was established a few years later, an economy already battling inflation was tipped into recession.

The embargo rattled more than the US economy; it challenged basic assumptions of American life, including our sense of entitlement to cheap and plentiful gasoline. Before the oil crisis, gasoline prices hovered around the mid-30-cent mark, with occasional local “gas wars” taking the price down to the high-20s--the inflation-adjusted equivalent of $1.60 per gallon now. Of course with average fuel economy around 13 miles per gallon, the effective real cost per mile wasn’t necessarily lower than today’s.

Within a year gas was over 50¢ at the pump, and by the end of the decade it passed $1.00/gal. for the first time. The gas lines that resulted from the unexpected supply shortfall and the federal government’s efforts to limit the ensuing increase in prices were an affront to drivers, a category that encompassed most of the over-16 population.

That first oil crisis and the subsequent energy crisis resulting from the Iranian Revolution in 1979 set in motion a number of important changes, including a sharply increased focus on energy efficiency, a deliberate effort to diversify our sources of imported oil, a pronounced shift away from oil in power generation — to the point that it now makes up less than 1% of US power plant fuel — and the beginnings of our search for affordable, renewable alternatives to oil.

The US Energy Security Council is an impressive group that includes many former government officials and captains of industry. They’ve clearly spent a lot of time studying this issue, and their report is worth reading. As I understand their conclusions and recommendations, they regard high oil prices as a bigger risk to the US economy than oil imports, per se, because of the impact of oil prices on consumer spending and the balance of trade. They have concluded that the most effective way to apply downward pressure on prices is not simply to reduce US oil imports, but to introduce meaningful fuel competition into transportation markets, where oil remains dominant with a share of around 93%.

The group doesn’t dismiss the benefits of increasing US oil production from sources such as the Bakken, Eagle Ford and other shale formations, but because these are relatively high-cost supplies, they have concluded that their leverage on global oil prices is limited. That means that higher US oil output couldn’t provide a path back to the price levels that prevailed before the Iraq War, when West Texas Intermediate crude averaged $26/bbl in 2002 and gasoline retailed for $1.35/gal.

This is a reasonable argument, though it’s worth considering that a return to $75/bbl might be feasible, if US production kept rising. That could yield US retail gasoline prices around $2.75/gal., equating to $2.15 in 2002 dollars. This isn’t as far-fetched as it might seem, because the global oil price is determined not by the entire 90 million bbl/day of world supply and demand, but by the last few million bbl/day of incremental supply, demand, and inventory changes.

The Council’s view also appears to emphasize the direct impact of oil prices on consumer spending without recognizing that rising production and falling imports shield the economy as a whole from the worst effects of high oil prices. With oil’s contribution to the trade deficit shrinking steadily, the main impact of higher oil prices is to divert money from consumers to shareholders of oil companies — of which I should disclose I am one. While exacerbating income inequality, that should at least result in a smaller impact on GDP and employment than the combination of rising oil prices and rising imports.

If the discussion had stopped at that point, the meeting would have been just another interesting Washington gabfest. However, the group’s analysis includes a set of actions it has identified as necessary for achieving their desired outcome: US energy security extending beyond the current US oil boom, underpinned by an expanding unconventional gas revolution that is widely expected to last for decades.

Their recommendations include giving fuels like methanol derived mainly from natural gas the chance to compete with gasoline made from oil, and with biofuels.They would start with revisions to the current US Corporate Average Fuel Economy standards to give carmakers incentives — not cash subsidies or mandates — to make at least half of all new vehicles fully fuel-flexible, capable of tolerating a wide range of blends of methanol, ethanol and gasoline. That seems like a no-regrets approach that could be achieved at a very low incremental cost per car. Even if you never bought a gallon of E85, M85, or M15, it could pay for itself by protecting your car from the damage that might result if you inadvertently filled up with gasoline containing more than the 10% of ethanol that carmakers believe is safe for non-flex-fuel cars. Other recommendations include easing regulations for retrofitting existing cars for flex-fuel and forming an alcohol-fuels alliance with China and Brazil.

Yet while I repeatedly heard that the group wasn’t promoting any single fuel, talk of methanol dominated the conversation. The moderator, Ann Korin, even joked that the session sounded like an “alcohol party.” As I later pointed out to her, there wasn’t a single mention of drop-in fuels — gasoline and diesel lookalikes derived from natural gas or biomass. I regard that as a crucial omission, because such fuels would be fully compatible with the billion cars already on the road, rather than just the 60 million or so new cars produced each year. They could provide greater leverage on oil prices by producing pipeline-ready products with which consumers are already familiar, from sources other than crude oil.

Part of the appeal of methanol seemed to be the potential for producing it from shale gas at a cost well below the cost of gasoline, even on an energy-equivalent basis — an important caveat, because a gallon of methanol contains half the energy of a gallon of gasoline. I hear the same argument in support of various pathways for producing jet fuel from non-oil sources, and it subscribes to the same fallacy: that market prices are set by manufacturing costs rather than supply and demand.

Fuel is a volume game. For a non-oil gasoline substitute to drive down oil prices –and thus motor fuel prices– as far as the Council apparently envisions, it would take at least several million barrels per day, on an oil-equivalent basis. Producing six million bbl/day of methanol from natural gas would consume 20 billion cubic feet per day of it. That’s 30% of last year’s US dry natural gas production, requiring 100% of the Energy Information Administration’s forecasted growth of US natural gas production through 2034. A number of other entities have their eyes on that same gas for other applications.

As many of the speakers at the Energy Security Council event reminded us, the world is a very different place than it was in 1973. Among other changes, US energy trends are headed in the right direction, with oil demand flat or declining, production rising and imports falling. That alone makes us more energy secure than we were, either five years ago or in 1972. Future oil supply disruptions are also unlikely to look much like the Arab Oil Embargo.

The Council is certainly correct that our unexpected shale gas bonanza, producing large quantities of new energy at a price equivalent to oil at $25 or less per barrel, provides a unique opportunity to weaken OPEC’s influence on oil prices. In pursuing that goal, however, it’s essential to remain flexible concerning the best pathways for gas to compete in transportation fuel markets, whether as CNG or LNG, or through conversion to electricity, methanol, or petroleum-product lookalikes. Consumer acceptance could prove to be the biggest uncertainty governing the ultimate outcome.

A different version of this posting was previously published on Energy Trends Insider.

Thursday, October 03, 2013

As US Oil Production Revives, New Vulnerabilities Appear

- The expansion of US oil production is centered in a handful of states, and in particular two whose gains more than offset declines in two former production leaders.

- For various reasons the West Coast has missed out on this revival, straining infrastructure and creating new vulnerabilities that should be addressed.

A handful of states still account for the lion's share of US oil production. Then and now, Texas tops the list, exceeding its 1989 output by 37%. At nearly 2.6 million barrels per day (MBD) in the most recent reported month --140% above at its low point in 2007--its share of US oil production had grown to around 35% by June. However, beneath Texas the list of top oil states has been jumbled in ways few would have anticipated two decades ago.

Alaska, California and Louisiana, the second-, third- and fourth-ranked producers in 1989, then supplied 41% of total US crude oil output. After decades of decline, the same three states now contribute just 17%, excluding production from the federal waters off Louisiana's coast.

Meanwhile, thanks to the development of the Bakken shale, North Dakota has jumped from the number 6 spot just five years ago to number two, eclipsing Alaska early in 2012. Traditional mid-tier producers like Colorado, Oklahoma and New Mexico are also contributing to the overall US oil revival. This surge of highly productive drilling in roughly the middle third of the country, on top of a million-plus barrels per day from the Gulf of Mexico --mainly from deepwater rigs--has scrambled existing oil transportation arrangements. |  |

When onshore production in Texas and the rest of the mid-Continent shrank in the 1990s and 2000s, the region's pipeline network gradually evolved into the country's principal oil-import conduit. The growth of production in the federal waters of the Gulf of Mexico, which had reached 1.6 MBD at the time of the Deepwater Horizon accident in 2010 but subsequently declined to about 1.2 MBD, meshed well with that model.

Today's big challenge goes against that grain: moving the growing surplus of oil in the upper plains states to markets on the West, Gulf and East Coasts, increasingly by rail. Much of the turbulence we've seen in the US oil market in the last two years reflects the delays inherent in realigning and expanding that network to accommodate newly abundant domestic supplies.

Yet on the other side of the Rockies, the picture looks very different. When I was trading crude oil for Texaco's west coast refining system in the late 1980s, balancing the crude oil surplus on the Pacific coast required shipping multiple tankers a month of Alaskan North Slope oil to the Gulf, where production was shrinking, and prompted the construction of a new pipeline to send surplus oil to east Texas over land. After two decades of decline from mature fields, along with moratoria on tapping new offshore fields, imports now make up roughly half of west coast refinery supply, even though regional petroleum demand is essentially back to 1989 levels. It remains unclear whether and when California will allow producers to tap the state's potentially game-changing oil resources in the Monterey shale deposit.

Barring further change, the regional nature of these shifts means that the energy security benefits accompanying the revival of US oil production are a party to which the West Coast has not been invited, or has perhaps declined the invitation. That's significant, because it leaves residents of California, Oregon, Nevada and Washington much more exposed to any disruptions in global oil trade, since the existing US Strategic Petroleum Reserve was never intended to provide coverage west of the Rockies. In this light, the appetite of west coast refiners for trainloads of Bakken and Eagle Ford crude looks strategic, rather than just a temporary response to market conditions.

A different version of this posting was previously published on the website of Pacific Energy Development Corporation.

Today's big challenge goes against that grain: moving the growing surplus of oil in the upper plains states to markets on the West, Gulf and East Coasts, increasingly by rail. Much of the turbulence we've seen in the US oil market in the last two years reflects the delays inherent in realigning and expanding that network to accommodate newly abundant domestic supplies.

Yet on the other side of the Rockies, the picture looks very different. When I was trading crude oil for Texaco's west coast refining system in the late 1980s, balancing the crude oil surplus on the Pacific coast required shipping multiple tankers a month of Alaskan North Slope oil to the Gulf, where production was shrinking, and prompted the construction of a new pipeline to send surplus oil to east Texas over land. After two decades of decline from mature fields, along with moratoria on tapping new offshore fields, imports now make up roughly half of west coast refinery supply, even though regional petroleum demand is essentially back to 1989 levels. It remains unclear whether and when California will allow producers to tap the state's potentially game-changing oil resources in the Monterey shale deposit.

Barring further change, the regional nature of these shifts means that the energy security benefits accompanying the revival of US oil production are a party to which the West Coast has not been invited, or has perhaps declined the invitation. That's significant, because it leaves residents of California, Oregon, Nevada and Washington much more exposed to any disruptions in global oil trade, since the existing US Strategic Petroleum Reserve was never intended to provide coverage west of the Rockies. In this light, the appetite of west coast refiners for trainloads of Bakken and Eagle Ford crude looks strategic, rather than just a temporary response to market conditions.

A different version of this posting was previously published on the website of Pacific Energy Development Corporation.

Thursday, June 20, 2013

It's Time To Reform US Ethanol Policy

- Virtually all of the assumptions underlying the Renewable Fuels Standard enacted in 2007 have changed, as the US emerges from energy scarcity into abundance.

- The linkage between the RFS and food prices is controversial, but a new quantitative model underscores concerns, especially for its impact on developing countries.

That requires a review of US fuel consumption and import trends, commodity prices, and the impact of the RFS on food prices. After summarizing the other points I want to focus on the last one, based on an interview I conducted with Dr. Yaneer Bar-Yam, an expert on complex systems who has developed a model that explains the behavior of food prices since the introduction of the first, less ambitious RFS in 2005.

In the fall of 2007, when Congress was debating the Energy Independence and Security Act that included the current, enhanced RFS, the US energy situation looked dire. For four years oil prices had been rising more or less steadily from their historical level in the low-to-mid $20s per barrel (bbl) to around $90, on their way to an all-time nominal high of $145/bbl the following summer. US crude oil production was in its 22nd consecutive year of decline, while our crude oil imports had climbed to 10 million bbl/day, twice domestic production that year.

Even more relevant to the thinking behind the RFS, US gasoline consumption stood at a record 142 billion gallons per year and had been growing at an average of 1.6% per year for the previous 10 years–another 2 billion gallons added to demand each year. In its annual long-term forecast for 2007, the Energy Information Administration (EIA) of the US Department of Energy had projected that gasoline demand would grow to 152 billion gal/yr in 2013 and 168 billion gal/yr by 2020. Meanwhile, US net imports of finished gasoline and blending components had reached a million barrels per day in 2006, equivalent to 15 billion gal/yr–equal to the corn ethanol target set by the 2007 RFS for gasoline blending in 2015. And by the way, US corn prices for the 2006-7 market year averaged $3.04 per bushel (bu). In this environment, policy makers regarded ethanol as a crucial supplement to dwindling hydrocarbon supplies, from a feedstock that was cheap and readily expandable.

Without belaboring the events of the last five years, virtually every one of those trends has reversed course. That has occurred partly as a result of the recession and the lasting changes it produced in the US economy, and partly due to an energy revolution that was largely invisible in 2007 but had already begun.

US gasoline consumption peaked in 2007 and has since declined to 133 billion gal/yr last year. The EIA forecasts it to fall to 128 billion by 2020 and 113 billion by 2030. US crude oil output is the highest in 22 years and is set to exceed imports this year, while the US has become a net exporter of gasoline and other petroleum products. Since 2007 US ethanol production has grown from 6.5 billion gal/yr to 13.3 billion gal., and it seems more than coincidental that corn prices had doubled to an average of $6.22/bu by last year.

That brings us to the controversy that has been widely referred to as “food vs. fuel”. In the last several years I’ve read numerous papers attempting to determine by correlation or other empirical methods whether and to what extent the increase in US ethanol production from corn has affected food prices. To put this in context, since 2005 the quantity of corn used for US ethanol production has grown from 1.6 billion bu/yr to 5 billion bu/yr, or from 14% to 40% of the annual US corn crop.

Some studies, such as this 2009 analysis from the non-partisan Congressional Budget Office found a significant influence on food prices. Others, including an Iowa State study recently cited in a blog post from the Renewable Fuels Association, found a negligible influence. What differentiates the work of Dr. Bar-Yam is that he and his colleagues have developed a quantitative model based on two key factors — corn consumed for ethanol and commodity speculation — that closely fits the behavior of a global price index. Their model also accounts for the “distillers dried grain” byproduct from ethanol plants, which returns about 20% of the corn used in the form of protein-upgraded animal feed.

Before speaking with Dr. Bar-Yam, I was a bit skeptical of his results. Aside from skepticism being my default mode in such situations, I had spent a lot of time looking at claims of speculator influence on crude oil prices in the 2006-8 period and was never convinced that they were more than the “foam on the beer”, rather than a basic driver of prices. However, as I was reviewing his paper prior to our call, a light went on.

The curve his model predicted, which closely matched food price behavior, looked very much like the behavior of a process control loop responding to a ramped change in the set point–forget the jargon and think about how the temperature of your home responds to a steady increase in your thermostat setting: overshooting, then undershooting, before converging. We discussed this and he confirmed that it was effectively an "under-damped oscillator", which can be characterized the same way whether you're talking about an electrical circuit or a market. In effect, the steadily increasing corn demand from the ratcheting up of the RFS started corn prices rising, and the presence of lots of speculators, including “index fund” investors, caused the price to successively overshoot and undershoot the equilibrium price track one would expect.

Dr. Bar-Yam explained that he had arrived at these two factors by eliminating factors that other groups had investigated, but that turned out to have no predictive value. These included shifting exchange rates, drought in Australia, a dietary shift in Asia from grains to meat, and linkages between oil and food prices. In his view the focus on ethanol and speculation is validated by the shift in dialog on this issue away from other, extraneous causes.

He also emphasized that his main concern is not the price of processed foods in developed countries such as the US, for which commodity grain costs are only one input, but rather the price paid for simple foods by poor people in the developing world. From that standpoint he doesn’t just want to see the RFS reformed. ”It is important not just to repeal, but to roll back the amount of ethanol used in the US.” He would prefer not 10% ethanol in gasoline, let alone 15%, but about 5%. “The narrative has to shift,” he said, “to recognize that people are going hungry.” Those are powerful words, and I’m still thinking about them.

At current production levels ethanol from corn contributes the energy equivalent of 6% of US gasoline consumption and about 2.5% of total US liquid fuel demand. That’s not trivial, and there’s a whole domestic industry of investors, employees and suppliers who made that happen at our collective request. However, If Dr. Bar-Yam has accurately captured the relationship between ethanol and global food prices, then we urgently need to reassess what we’re doing with this fuel.

We are also in a far better position now to consider scaling back our use of ethanol produced from grain than we were when the RFS was established. With increasing production of shale gas, tight oil and various renewables, the energy scarcity that has defined our policies for the last four decades is far less relevant to our policy choices going forward. I’ll tackle the practical aspects of RFS reform, in terms of the so-called “blend wall” and its impact on gasoline prices, in a future post.

A slightly different version of this posting was previously published on Energy Trends Insider.

Thursday, April 11, 2013

The White House 2014 Budget Energy Proposals: Stuck in A Timewarp

- The President's budget proposal would increase taxes on energy in ways that would harm US competitiveness and consumers.

- Presenting the Energy Security Trust as a zero-sum game undermines its potential effectiveness and bi-partisan appeal.

After spending some time going through the White House's proposed budget for 2014-23, several conclusions were inescapable. First, this administration still hasn't thought through the implications of the energy revolution that's currently unfolding in the US, as a result of the technology to develop our enormous shale oil and gas resources, which grew even larger this week. Not satisfied to see tax revenues and royalties from oil and gas expand as production grows, they miss no opportunity to seek to slice more from the current pie. This failure of imagination extends to the proposed Energy Security Trust Fund, which sounded intriguing when President Obama mentioned it in this year's State of the Union speech, but now appears to be mainly an accounting gimmick based on a zero-sum mentality. Meanwhile, the budget's proposals for renewable energy and advanced technology vehicles seem largely divorced from our experience of the last several years.

Let's start with the tax changes and quickly dismiss them, because they're mostly a rehash of provisions in the administration's last four budgets and stand no better chance of Congressional approval this side of comprehensive tax reform. Once again, we see proposals to eliminate about $4 B per year worth of tax treatment for the oil and gas industry, including provisions like the Section 199 deduction enjoyed by all US manufacturers. Now add proposed changes in the treatment of foreign taxes, which would subject this highly international industry to double taxation on its activities outside the US, under the misappropriated label of "reform." (True reform would move toward the territorial system used by most advanced economies.) Finally, the President's budget would eliminate both the widely used last-in, first-out (LIFO) and lower-of-cost-or-market (LCM) methods of cost accounting for inventories. I don't know how much of the $87 B of higher revenue over ten years ascribed to that shift would come from the oil and gas industry, but it would certainly be in the billions, if this weren't all dead on arrival.

That brings me to the Energy Security Trust Fund, described in the State of the Union as a way to employ revenue from oil and gas development to fund R&D on reducing our dependence on oil. That looked clever, if applied to incremental resource opportunities. More production would fund more research, in an almost virtuous cycle. Yet that's not how the idea would be implemented in this budget. Instead of opening up new areas for drilling, and earmarking the royalties that would generate, the $2 B for the Trust would come mainly from diverting royalties from leases already in the budget, and from further "reform": higher royalties on US production and higher rentals and shorter lease terms to provide "incentives to diligently develop leases." The latter echoes the "idle leases" canard we've heard since 2008, reflecting a continued misunderstanding of how the industry actually works, along with the real-world factors that often impede faster lease development, such as permitting delays and lawsuits.

So at least this part of the President's "all of the above" energy agenda is reduced to measures that, rather than "encouraging responsible domestic energy production", would make the US a much less attractive place to invest in developing oil and gas resources, and likely reverse our recent successes. Yet if the new budget treats conventional energy as a slush fund to be raided, renewables and efficiency are treated to what would amount to a reprise of the 2009 stimulus. I tallied $39.8 B through 2023 for programs such as alternative fuel vehicles, advanced technology vehicle manufacturing, advanced energy equipment manufacturing, bioenergy crop assistance, home energy efficiency retrofit credits, efficient buildings, and the Energy Security Trust Fund. 44% of the total would go to a single measure: making the production tax credit (PTC) for wind and other renewable energy permanent, instead of phasing it out, as even the American Wind Energy Association has suggested. That's a bad idea for two reasons.

First, it ignores a growing body of analysis pointing to the need for significant innovation in wind, solar and other renewable energy technologies, rather than continuing to pay project developers indefinitely to deploy the current technologies. It also exposes a basic logical flaw in the argument for more subsidies: Renewables cannot simultaneously be approaching the point of becoming competitive with conventional energy, as they must if they are to capture significant shares of the energy market--wind accounted for 3.5% of US net electricity generation last year, and solar just 0.1%--while still needing permanent subsidies at rates orders of magnitude higher, on an energy-equivalent basis, than the tax breaks for oil & gas that the administration seeks to end.

After four years in office, it's reasonable to expect an administration to have learned what works and what doesn't. The President and his officials seldom miss an opportunity to brag about the enviable record of oil and gas production growth that has occurred since 2008, yet continue to propose and enact policies that, had they been in place in the previous decade--when the seeds of this growth were actually planted in an environment of rapidly rising energy prices--might well have nipped that growth in the bud. Nor do they seem to have learned much from the track record of business failures that has dogged their efforts in the renewable energy and advanced vehicles space--a record that extends well beyond the over-used example of Solyndra. Taxing oil and gas much harder won't lead to more US production, nor will handing investors additional billions in taxpayer funds make renewables and electric vehicles competitive, without significant further improvements in the technologies.

Thursday, September 06, 2012

What If Saudi Arabia Became an Oil Importer?

I've seen numerous references in the last several days to a Citgroup analysis suggesting that Saudi Arabia might become a net oil importer by 2030. The premise behind this startling conclusion seems to be that economic growth and demographic trends would continue pushing up domestic Saudi demand for petroleum products and electricity--generated to a large extent from petroleum--until it consumed all of that country's oil export capacity within about 20 years. Even if this trend didn't proceed to conclusion, its continued progression could significantly alter both global oil markets and the context for the current debate about the desirability of achieving North American energy independence.

I'd be a lot more comfortable discussing this news item if I had access to the report on which it's based. Unfortunately, none of the dozens of references to it that I found on the web included a link to the source, which is probably on one of Citi's client-only sites. The Bloomberg and Daily Telegraph articles seemed to be the most complete, with the latter including a couple of charts from the report. As best I can tell, the analysis falls into the category of "If this goes on" scenarios--extrapolations of currently observable trends to some logical conclusion. That doesn't make it simplistic, because I'm sure the author sifted through volumes of data to flesh it out. The fact that many oil-producing countries have gone through a similar cycle lends it further credibility. For that matter, the US was once an important oil-exporting country, until the growth of our economy overwhelmed the productivity of US oil fields early in the last century. The gradual conversion of the remaining oil exporters to net oil consumers is a basic plank of the Peak Oil meme.

This presents a real conundrum, both for the Saudis and for us, because although many of the means by which this result could be averted are obvious, they aren't all feasible within the current political situation in Saudi Arabia, or indeed many other producing countries. Start with per-capita energy consumption, which a chart in the Telegraph article shows to be higher than in the US. Consumption is also high relative to GDP. Energy efficiency opportunities should be ample, but it's hard to make those a priority when retail energy is heavily subsidized and thus cheap. The Citigroup report apparently suggests reducing energy subsidy levels, but that might lead to the same kind of unrest that we've seen in other countries that have cut subsidies. That seems to leave mainly investment-based options for substituting other energy sources for oil, to preserve oil for exports. The Kingdom has already embarked on some of these, including nuclear and solar power. When combined with additional natural gas development, the Saudis certainly have the means and the motivation to shift the current trend of rising internal oil consumption, along with the cash to fund the infrastructure investment involved.

This leaves us with important strategic questions: To what extent should our own energy policy rely on Saudi Arabia succeeding in preserving its oil export capacity by means of substitution or efficiency gains? And if internal Saudi consumption removed just another 2-3 million barrels per day of exports from the market, how would that affect oil prices and the functioning of the global oil market, in which Saudi Arabia has often acted as a moderating force within OPEC? Considering that a narrowing between demand and available supply of about that magnitude was a key factor in the oil-price run-up of 2006-8, this should cause us serious concern.

That brings us to US energy independence, a tired mantra that has been proclaimed by a long succession of US Presidents, despite most experts for the last several decades having regarded it as unrealistic. To be clear, when Americans speak of energy independence, we are referring to oil, because as a practical matter that's the only form of energy we import to any significant degree, if you don't count natural gas from Canada. Yet suddenly energy independence no longer looks like a pipe dream, because of the combination of resurgent domestic oil production and improvements in vehicle fuel efficiency. An earlier report from Citigroup sketched the outline of potential future North American energy independence based mainly on those elements. It's hardly guaranteed, but it's not a fantasy, either.

Despite the risks of a much more unsettled oil market in the future, I continue to see a great deal of misunderstanding about what energy independence could mean for the US. Although it wouldn't cut us off from the global oil market--perish the thought--it would give us a much more flexible and influential role within it, while taking advantage of the benefits of continued trade. No longer being a net oil importer wouldn't insulate us from future oil price movements--it's still a global commodity--but oil prices would be lower than otherwise as a direct result of the substantial additions to supply required to shrink US oil imports to near zero. Prices would be weaker even if OPEC slashed output to compensate, because the resulting increase in spare production capacity would still reduce market volatility. Moreover, while US energy independence would not preclude the possibility of future oil price spikes, the consequences of those would be very different. For starters, they wouldn't entail weakening our economy by transferring tens or hundreds of billions of dollars offshore. Most of the extra oil revenue would stay in the US, and a large slice of it would be captured by state and federal taxes and royalties. Contrast that with what happened in 2008, and is still ongoing to a lesser degree.

The Saudi analysis from Citigroup proposed a fascinating scenario, with many interesting implications, although I'd argue that it's also subject to the simple advice of Herb Stein that "If something cannot go on forever, it will stop." By coincidence, it's also relevant to the energy debate underway between the US presidential campaigns. Although it's highly uncertain that Saudi Arabia's oil exports will dry up by 2030, we shouldn't assume such an outcome to be impossible, any more than we should base US energy policy on the outdated assumption that it's impossible for us to come close to eliminating the need for oil imports from outside North America. It might be uncertain whether we have sufficient resources accessible with the latest technology to reach that goal, but it is essentially certain that the growing but still tiny contribution of renewable energy and the eventual conversion of the US vehicle fleet to electricity couldn't get us there for multiple decades.

I'd be a lot more comfortable discussing this news item if I had access to the report on which it's based. Unfortunately, none of the dozens of references to it that I found on the web included a link to the source, which is probably on one of Citi's client-only sites. The Bloomberg and Daily Telegraph articles seemed to be the most complete, with the latter including a couple of charts from the report. As best I can tell, the analysis falls into the category of "If this goes on" scenarios--extrapolations of currently observable trends to some logical conclusion. That doesn't make it simplistic, because I'm sure the author sifted through volumes of data to flesh it out. The fact that many oil-producing countries have gone through a similar cycle lends it further credibility. For that matter, the US was once an important oil-exporting country, until the growth of our economy overwhelmed the productivity of US oil fields early in the last century. The gradual conversion of the remaining oil exporters to net oil consumers is a basic plank of the Peak Oil meme.

This presents a real conundrum, both for the Saudis and for us, because although many of the means by which this result could be averted are obvious, they aren't all feasible within the current political situation in Saudi Arabia, or indeed many other producing countries. Start with per-capita energy consumption, which a chart in the Telegraph article shows to be higher than in the US. Consumption is also high relative to GDP. Energy efficiency opportunities should be ample, but it's hard to make those a priority when retail energy is heavily subsidized and thus cheap. The Citigroup report apparently suggests reducing energy subsidy levels, but that might lead to the same kind of unrest that we've seen in other countries that have cut subsidies. That seems to leave mainly investment-based options for substituting other energy sources for oil, to preserve oil for exports. The Kingdom has already embarked on some of these, including nuclear and solar power. When combined with additional natural gas development, the Saudis certainly have the means and the motivation to shift the current trend of rising internal oil consumption, along with the cash to fund the infrastructure investment involved.

This leaves us with important strategic questions: To what extent should our own energy policy rely on Saudi Arabia succeeding in preserving its oil export capacity by means of substitution or efficiency gains? And if internal Saudi consumption removed just another 2-3 million barrels per day of exports from the market, how would that affect oil prices and the functioning of the global oil market, in which Saudi Arabia has often acted as a moderating force within OPEC? Considering that a narrowing between demand and available supply of about that magnitude was a key factor in the oil-price run-up of 2006-8, this should cause us serious concern.

That brings us to US energy independence, a tired mantra that has been proclaimed by a long succession of US Presidents, despite most experts for the last several decades having regarded it as unrealistic. To be clear, when Americans speak of energy independence, we are referring to oil, because as a practical matter that's the only form of energy we import to any significant degree, if you don't count natural gas from Canada. Yet suddenly energy independence no longer looks like a pipe dream, because of the combination of resurgent domestic oil production and improvements in vehicle fuel efficiency. An earlier report from Citigroup sketched the outline of potential future North American energy independence based mainly on those elements. It's hardly guaranteed, but it's not a fantasy, either.

Despite the risks of a much more unsettled oil market in the future, I continue to see a great deal of misunderstanding about what energy independence could mean for the US. Although it wouldn't cut us off from the global oil market--perish the thought--it would give us a much more flexible and influential role within it, while taking advantage of the benefits of continued trade. No longer being a net oil importer wouldn't insulate us from future oil price movements--it's still a global commodity--but oil prices would be lower than otherwise as a direct result of the substantial additions to supply required to shrink US oil imports to near zero. Prices would be weaker even if OPEC slashed output to compensate, because the resulting increase in spare production capacity would still reduce market volatility. Moreover, while US energy independence would not preclude the possibility of future oil price spikes, the consequences of those would be very different. For starters, they wouldn't entail weakening our economy by transferring tens or hundreds of billions of dollars offshore. Most of the extra oil revenue would stay in the US, and a large slice of it would be captured by state and federal taxes and royalties. Contrast that with what happened in 2008, and is still ongoing to a lesser degree.

The Saudi analysis from Citigroup proposed a fascinating scenario, with many interesting implications, although I'd argue that it's also subject to the simple advice of Herb Stein that "If something cannot go on forever, it will stop." By coincidence, it's also relevant to the energy debate underway between the US presidential campaigns. Although it's highly uncertain that Saudi Arabia's oil exports will dry up by 2030, we shouldn't assume such an outcome to be impossible, any more than we should base US energy policy on the outdated assumption that it's impossible for us to come close to eliminating the need for oil imports from outside North America. It might be uncertain whether we have sufficient resources accessible with the latest technology to reach that goal, but it is essentially certain that the growing but still tiny contribution of renewable energy and the eventual conversion of the US vehicle fleet to electricity couldn't get us there for multiple decades.

Subscribe to:

Comments (Atom)