- Current debates over LNG export often ignore its primary benefits, such as enabling gas to be produced for sale to markets beyond the realistic reach of pipelines.

- It also allows gas to compete with petroleum liquids where energy density is important, such as in powering ships, trains and land vehicles.

The big driver for this is economic: UK Brent crude is currently over $100 per barrel, while natural gas in the US Gulf Coast trades at the energy equivalent of around $25 per barrel. That creates a significant incentive to build LNG plants, despite the recent escalation in their cost. Even after adding the equivalent of $20-30/bbl in expenses for liquefaction, shipping, and regasification to convert the LNG back into pipeline gas at its destination, the opportunity is significant. In Asia, where LNG sells for $14 or $15 per million BTUs, that's still less than $90 per equivalent barrel. And because gas can only be produced if it can be connected to a market, LNG enables more gas to compete in more markets, while providing customers a cleaner and cheaper fuel.

This is not a new technology. Early demonstrations in the 1940s and '50s were followed by commercial-scale plants built to export LNG from Alaska, Algeria and Indonesia, establishing what has since become a global industry. Every LNG plant is designed to take advantage of the fact that at atmospheric pressure natural gas becomes a liquid at -259 °F ( -161 °C)--about 60°F warmer than liquid nitrogen--shrinking by a factor of 600:1 in the process. As long as it is kept below that temperature, it can be stored and transported as a liquid.

That has important advantages over the alternative of compressing natural gas to create a denser fuel. For example, a gallon of LNG has around 2.2 times as much energy (based on lower heating values) as the same volume of compressed natural gas (CNG) at 3,000-3,600 pounds per square inch (psi). A gallon of LNG also has 98% of the energy of ethanol, and 64% that of gasoline. This makes LNG dense enough to transport economically over long distances, unlike CNG.

These differences have a practical impact on the gradual penetration of the transportation fuel market by natural gas. While most natural gas passenger cars are based on the simpler CNG approach, LNG is gaining a foothold in trucking, particularly where the combination of low emissions and denser fuel--yielding longer range--is important.

LNG is also emerging as an option for transportation modes that have had few viable alternative to oil-based fuels, such as in shipping and even rail where electrification is impractical. Replacing ships' bunker fuel with LNG could be a key strategy for responding to increasingly strict international regulations on sulfur and nitrogen oxide pollution from ocean-going vessels.

The environmental benefits of LNG can be significant, when it replaces higher-emitting fuels like coal and fuel oil. Even after accounting for the energy consumed in the liquefaction process-- equivalent to 8% or less of the gas input to a new LNG plant--and in storage and transportation, lifecycle emissions from LNG in power generation are 40-60% lower than those from coal. Its advantage in marine engines is smaller, but still positive at around 8%, while reducing local pollution significantly.

LNG isn't without drawbacks, including "boil-off", the gradual tendency of LNG in storage to evaporate due to heating from the environment outside the insulated tank. In stationary facilities the resulting gas can either be re-liquefied or delivered to meet local gas demand. In vehicles, it is vented after a specified holding time of around a week or more. That makes it more suitable for vehicles that are used frequently, rather than sitting idle for extended periods.

It's worth noting that while LNG is increasingly linked to shale gas in North America, nearly all the LNG currently marketed around the world is produced from conventional gas reservoirs, such as the supergiant North Field in Qatar, or the gas fields of Australia's North West Shelf. That would also be the case for a new LNG plant based on Alaskan North Slope gas, as described in a post here in 2012.

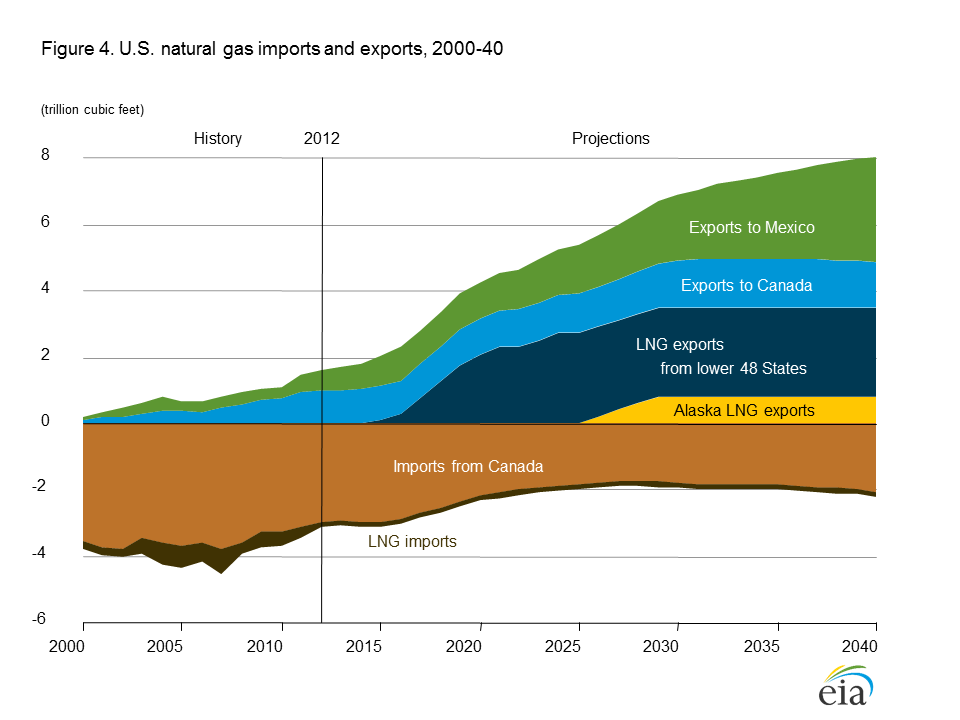

Only a few years ago, government and industry forecasts were unanimous in projecting a large and growing US LNG import requirement, as domestic gas production declined. The number of US LNG import facilities expanded to meet this new demand, but the combination of the recession and the shale gas revolution has resulted in imports shrinking substantially since 2007. The Energy Information Administration now expects the US to become a net exporter of LNG in 2016, including exports from repurposed import facilities. They will join a market that now supplies around 10% of global natural gas consumption and accounts for a third of global gas trade.

A different version of this posting was previously published on the website of Pacific Energy Development Corporation.

{kind=link}

{kind=link}

_in_thousand_terajoules_(GCV)-tb1.png&filetimestamp=20130625095947){kind=link}

{kind=link}

{kind=link}