When President Trump announced last week that the US would withdraw from the Paris Climate Agreement, he unleashed a flood of condemnation. Foreign leaders, US politicians, corporate executives, and environmental groups all roundly criticized the move. It also hasn't polled well.

As the initial reaction dies down, it's worth considering how this happened, what it means, and what might come next. The invaluable Axios news site has some noteworthy insights on the latter problem that I will get to shortly.

I am convinced it was a mistake to withdraw. In this I share the view of many current and former business leaders, including the Secretary of State, that the US was better off as a party to the deal and all the future negotiations it entails. Even if the goal was truly to renegotiate the agreement on more favorable terms, signaling withdrawal first seems counterproductive. However, I also see the consequences of our withdrawal in less catastrophic terms than most critics of the move.

As I noted not long after it was concluded, the Paris Agreement is by design much weaker than its predecessor, the Kyoto Protocol. Although the 2015 Paris deal was probably the strongest one that could have been negotiated at the time, it still represented a big compromise between developed and developing countries on who should reduce the bulk of future emissions and who should bear the responsibility for the consequences of past emissions. Its text is full of verbs like recognize, acknowledge, encourage, etc., and the commitments it collected were essentially voluntary.

The agreement was also explicitly negotiated so as to maximize its chances of being enacted under the executive powers of the US president, without his having to refer the agreement to the US Senate for its concurrence. That implied it could be undone in the same way.

In other words, President Obama took a calculated risk that his successor(s) would choose to be bound by his Executive Order endorsing Paris. That was tantamount to a bet on his party winning the 2016 election, since most of the Republicans who had announced at the time were opposed to it, or the Clean Power Plan that was the linchpin of future US compliance with it.

Seeking Senate approval as a treaty would have been a much bigger lift--or required an even weaker agreement--but success would have provided significant political protection for the follow-on to the unratified Kyoto Protocol. Perhaps that explains why President Trump has chosen the much slower exit path--up to three years--provided within the Paris Agreement, rather than the quicker route of pulling out of the umbrella UN Framework Convention on Climate Change. The Convention was signed by President George H.W. Bush with the bipartisan advise and consent of the Senate in 1992.

Setting politics aside, it's also not obvious that US withdrawal from Paris will put our greenhouse gas emissions on a significantly different track than if we stayed in. Even the EPA's review and likely withdrawal of its previous Clean Power Plan, which underpinned the Obama administration's strategy for meeting the voluntary goal it submitted at Paris, may have only a minor impact on global emissions.

Federal climate policy has not been the main driver of recent emissions reductions in the US power sector. Cheap, abundant natural gas from shale and the rapid adoption of renewable energy under state "renewable portfolio standards", supported by federal tax credits that were extended again in 2015, have been the primary factors in overall US emissions falling by 11% since 2005. These trends look set to continue.

The bigger question is what happens globally with the US out of the Paris Agreement--assuming the administration does not reverse course again before it can issue the required formal notice to withdraw roughly 2 1/2 years from now.

At least in the short term, I doubt much else will change. For the most part, the Nationally Determined Commitments delivered at Paris reflected what the signatories intended to do anyway. China's NDC is a perfect example. That country's ongoing air pollution crisis provides ample incentive to scale back on energy intensity and coal-fired power plants, which are the main source of its emissions.

Increasing the role of renewable energy in its national energy mix perfectly suits China's ambitions in renewable energy technology. Exhibit A for that is a solar manufacturing sector that went from insignificance to more than 50% of the global supply of photovoltaic (PV) cells in under a decade, while China's domestic market accounted for 21% of global PV installations through 2015.

The reactions to last week's announcement surely raised the stakes for other countries that might consider leaving. However, this action has also provided China and other high-emitting developing countries with an ironic mirror image of one of the main arguments on which the US government based its unwillingness to implement the Kyoto Protocol.

What ought to matter more than any of the domestic and geopolitical maneuvering around the US exit is the actual impact on the global climate. Reporting on Axios, Amy Harder (formerly of the Wall St. Journal) portrayed this as a sort of emperor's clothes moment with a column entitled, "Climate change is here to stay, so deal with it." Monday's main Axios "stream" characterized her piece as a "truth bomb."

As Harder put it, "The chances of reversing climate change are slim regardless of US involvement in the Paris agreement." That's consistent with recent assessments from the International Energy Agency and others. Citing the Bipartisan Policy Center and the UN, her column suggested a pivot to greater focus on adaptation, the hard and deeply unglamorous work of bolstering infrastructure and systems to withstand changes in the climate, including those that are already baked in. Attributing the source of changes in rainfall and sea level matters less than plugging the resulting physical gaps. That makes adaptation politically less toxic than cutting emissions, though still plenty challenging, fiscally.

As I have been watching the fallout from last week's news, I keep coming back to comparisons to the Cold War that I made when the idea of pursuing climate policy through executive action was emerging in 2010. Like the Cold War, dealing with climate change requires a similarly enduring bipartisan coalition. Major policy swings every 4 or 8 years are just too costly and ineffective, due to the planning horizons involved.

NATO may be going through a difficult moment, but it is approaching its 70th year. After seeing its key weakness exposed, can anyone honestly look at the framework of the Paris Agreement and conclude that it is likely to last as long? Yet if climate change is as serious as many suggest, those are exactly the terms in which we should be thinking.

Showing posts with label Paris COP. Show all posts

Showing posts with label Paris COP. Show all posts

Tuesday, June 06, 2017

Thursday, January 12, 2017

US Energy Under Trump

- President-Elect Trump and his appointees plan a major policy and regulatory shift for energy, focusing more on economic benefits and less on environmental impacts.

- Obama-era regulations most at risk of roll-back are those justified mainly on climate concerns not shared by Mr. Trump and his team.

- Emissions are still likely to fall in the next four years as shale and renewable energy output grow.

To gauge how sharply the energy polices of the incoming Trump administration will diverge from those of the last eight years, we need to understand what motivates both leaders. The Obama administration's approach was driven by a deep, shared conviction that climate change is the most important challenge the US--and world--faces. The cost of energy and its impact on the economy became secondary concerns, subordinated by the belief that the added cost of climate policies would be offset in whole or part by the benefits of the green investment they unleashed--remember "green jobs"?

We saw this in President Obama's first year in office. Amid a deep recession he worked with Congress to attempt to limit greenhouse gas emissions by means of an economy-wide cap-and-trade system, on which he had campaigned. The House of Representatives passed the Waxman-Markey bill (HR.2454), a veritable dog's breakfast of economic distortions. Yet despite a filibuster-proof majority in the Senate in 2009, Waxman-Markey and every subsequent cap-and-trade bill died there.

That failure set in motion the agenda that the Obama administration has pursued ever since, to achieve via regulations the emissions reductions it could not deliver through comprehensive climate legislation. Last year's publication of the EPA's final Clean Power Plan was a key component of an effort that seems set to continue until just before Inauguration Day.

The transformation of energy regulations under President Obama was dramatic enough that a transition to any Republican administration would be a big change. The transition now in prospect will be even more jarring. Mr. Trump's rhetoric and his choices for key administration positions point to a concerted effort to unravel as many of the Obama-era regulations affecting energy as possible. That isn't just based on philosophical differences over regulation and markets. For President-Elect Trump the economy and jobs are paramount, so the Obama energy regulations must look like an unjustifiable threat to the fossil fuel supplies that still meet 81% of the nation's energy needs.

Despite that, it is unlikely the new administration will go out of its way to target renewable energy or the tax credits that have driven its growth to date. Renewables are becoming increasingly popular with conservatives. However, because Mr. Trump sees climate change as, at best, a secondary issue that may not be amenable to human intervention, his administration's won't put renewables on a pedestal as the Obama administration has done.

The biggest challenge for renewable energy may come from tax reform intended to make US companies and factories more competitive globally and shrink the incentive for them to relocate to lower-tax countries. This appears to be a high priority for the new White House and Congress, and one on which they broadly agree. If corporate tax rates drop, the value of the tax credits renewables enjoy is likely to fall, too, making wind, solar and other such projects less attractive and less competitive.

It remains to be seen how many of the Obama energy regulations can be rolled back. The most recent regulations might be averted through legislation like the Midnight Rules Relief Act, or the REINS Act, both of which would update the Congressional Review Act, a rarely used 1990s law intended to limit what presidents could impose by last-minute executive actions. Other regulations may eventually stand or fall as the courts rule. The stakes are high, particularly for regulations affecting the production of oil and gas from shale by means of hydraulic fracturing and horizontal drilling.

Energy independence was a touchstone of Mr. Trump's candidacy. Despite his campaign's focus on coal, it is fracking, as hydraulic fracturing is more commonly known, that holds the key to achieving that goal in the foreseeable future. It has been the main driver of the growth in US energy production since 2010.

The latest long-term forecast from the US Energy Information Administration (EIA) puts energy independence within reach--in the sense of the US becoming a net exporter of energy--by 2026 or sooner. However, the recent flurry of regulations affecting such things as drilling on federal land, and putting large portions of US waters off-limits for offshore drilling would not have been part of that projection. As EIA Administrator Adam Sieminski remarked at a briefing on the forecast, "If you had policy that changed relative to hydraulic fracturing, it would make a big, big difference to everything that's in here."

That's a key point, because most past notions of energy independence assumed that energy prices would have to be very high to promote lots of efficiency and conservation and stimulate large amounts of expensive new supply. The shale revolution changed that.

However, the global context is also changing. OPEC is attempting to reassert its control over the oil market, with help from non-OPEC countries like Russia. Two years of low oil prices shrank global oil and gas investment budgets by around a trillion dollars, and the International Energy Agency has warned of coming oil price spikes as a result. Forestalling tighter US regulations on fracking and offshore drilling increases the chances that US supplies could grow by enough to balance shortfalls elsewhere and avert much higher prices at the gas pump.

Energy infrastructure is likely to be another focus of the new administration, because the economic and competitive benefits of abundant energy will be diluted if, for example, Marcellus and Utica shale gas or Bakken and Permian Basin shale oil have to be exported because domestic customers don't have access to them.

That suggests an early effort to reverse decisions by the current administration to block the construction of various pipelines, starting with the Keystone XL pipeline and more recently the Dakota Access Pipeline. That will force new confrontations with activists and environmental organizations that have raised their game to a new level in the last eight years.

Such opposition would likely intensify if the new administration sought to withdraw the US from the Paris climate agreement, which recently went into effect, or submitted it for review by the US Senate as a treaty. But it's not clear that a big change in direction would require leaving Paris.

The US commitments at Paris, like those of the other signatories, were voluntary and non-binding. For that matter, recent shifts in US energy consumption and especially electricity generation have put the US in a good position to meet its initial Paris goals with little or no additional effort, as noted by outgoing Energy Secretary Moniz. The Paris Agreement will only become a major point of contention if President Trump chooses to make it one.

In his list of the top energy stories of 2016, fellow blogger Robert Rapier rated the election of Donald Trump ahead of the OPEC deal and many other important events of the year, based on its likely impact on "every segment of the US energy industry." In retrospect that was equally true of Barack Obama's election in 2008. The shift we are about to experience on energy will be that much sharper, because President Obama and President-Elect Trump both set out to make big changes to the status quo for energy, in opposite directions. We shouldn't miss one important difference, however.

The course that Barack Obama's administration followed on energy was largely predictable from the start, because it was based on openly and deeply held beliefs about energy and the environment. Donald Trump's well-known preference for deals over dogma sets up the prospect of some big surprises, in addition to what we can already anticipate.

Thursday, November 03, 2016

Energy and the 2016 Presidential Election

In less than a week, the most controversial and acrimonious presidential election in living memory will be over. Energy has largely been a second-tier issue in this contest, although the divergence in the candidates' views on this vital subject is stark. Fortunately, the energy consequences--planned and unintended--of the last two US presidential elections hold some useful lessons for considering the proposed energy policies of this year's two front-runners.

As we look back, please recall that for most of the 2008 campaign the average US price for unleaded regular gasoline was over $3.00 per gallon. Much of that summer it was at or above $4.00. Four years later, from Labor Day to Election Day of 2012, regular gasoline averaged $3.76 per gallon. The comparable figure for the last two months of the 2016 campaign is just under $2.25.

In 2008 energy independence was a hot issue. Then-Senator Obama ran on a platform that targeted reducing US oil imports by over 3 million barrels per day, mainly through improved fuel efficiency. In his view US oil resources were effectively tapped out--remember "3% of reserves and 25% of consumption"? The main role he envisioned for the US oil and gas industry was as a source of increased tax revenue. His primary focus was on reducing greenhouse gas emissions through large federal investments in green energy technology. He would soon deliver on that promise with the $31 billion renewable energy package included in the federal stimulus of 2009.

When he was running for reelection in 2012, President Obama had kinder words for conventional energy, particularly the large expansion of US natural gas supply due to shale gas. He even took credit for "boosting US domestic production of oil". That point provoked an extended argument in the second presidential debate that year. Importantly, when the President emphasized renewable energy, energy efficiency and emissions, it was within a broader framework of "all of the above" energy.

At the same time, following the failure of comprehensive energy and climate legislation in his first term, his administration has pursued major new regulations aimed at achieving its energy and environmental goals. However, some of the most sweeping of these, including the Clean Power Plan, have gotten hung up in the courts, while others have yet to be fully implemented.

In retrospect President Obama was lucky. The shale energy revolution wasn't on his radar in 2008 and received little or no help from his administration, but it has increased US energy production by more than 17%, net of coal's losses, since he took office. It has made a major dent in US oil imports and CO2 emissions. In the process, it saved consumers hundreds of billions of dollars on their energy bills, reduced the US trade imbalance, generated large numbers of new jobs when it mattered most, and provided the primary means for reducing US greenhouse gas emissions to their lowest level since before Bill Clinton ran for President.

Meanwhile, the renewable energy revolution on which his 2008 campaign pinned most of its hopes is still a work in progress. The cost of non-hydro renewables, mainly wind and solar power, has fallen dramatically and their deployment has grown impressively, expanding by a combined 135% from 2008 to 2014, or 15% per year. Wind and solar power are reshaping US electricity markets and changing the economics of baseload power plants, including nuclear plants. However, these sources still generate just 8% of US electricity and accounted for less than 3% of total US energy production in 2015.

What can we learn from the experience of the last two presidential terms? We are certainly in the midst of a long-term transition from a high-carbon energy economy to one using lower-carbon fuels and low- or effectively zero-carbon electricity. However, the numbers tell us that with regard to implementation, if not technology, we are closer to the beginning of that transition than to its end. The next President can double renewables, and that would still leave us reliant on conventional energy and nuclear power for three-quarters of our electricity and 90% of our total energy needs.

Going from 3% of energy from new renewables to the levels needed to meet the emissions targets that the US took on at Paris last year represents an enormous technical and financial challenge. It won't happen without a healthy economy, supported by a diverse and flexible energy mix anchored by domestic oil and natural gas from public and private lands and waters.

Although the Obama administration has added numerous regulations affecting energy, it stopped short of derailing the shale revolution. As a result, it has benefited greatly from the increased flexibility and energy security shale is providing. President Obama adapted his approach to energy and came around to recognizing the need for an energy mix that balances new, green energy with the best conventional energy sources. That's the lens through which we should view the energy proposals of this year's candidates.

There's no question that Secretary Clinton would promote the continued growth of renewable energy and the wider application of energy efficiency. If anything, she seems to be even more focused on climate change and clean energy than Barrack Obama was in 2008. However, her campaign website portrays oil and gas mainly in negative terms, with a focus on cutting their consumption, along with the industry's tax benefits. While explicitly recognizing the role that increased US natural gas production has played in reducing emissions, her policies would directly target the primary source of that growth.

Shale gas now accounts for half of all US natural gas production, but Secretary Clinton is on record supporting much stricter regulations on "fracking", the common shorthand for the technological processes involved in producing oil and gas from shale: "By the time we get through all of my conditions, I do not think there will be many places in America where fracking will continue to take place,” she said in a March debate with Senator Sanders.

Reversing the recent growth of natural gas production from shale would lead to higher emissions during the next four to eight years. With less gas available, natural gas prices would rise, and the remaining coal-fired power plants would ramp back up to fill the gap, even as renewables continued to expand. That is happening in Germany today as that country turns away from nuclear power. In the US, without the contribution from natural gas and nuclear power plants, another of which just shut down permanently, our climate goals would be out of reach.

Recently, Secretary Clinton was also cited as wanting to expand the current administration's moratorium on coal development from public lands to encompass oil and gas. As shown in the chart below, based on data from the US Energy Information Administration, this production is already trending downward, overall. Imposing a moratorium on oil and gas development on public lands would accelerate that contraction, without new wells to offset the decline from mature fields.

If implemented as described, Secretary Clinton's policy toward shale energy would have an even more pronounced effect on US energy supplies than restricting development on federal land. With oil prices low, shale oil production has already fallen by 1.2 million barrels per day since output peaked in May 2015. The drop would have been much steeper had US producers not been able to focus their greatly reduced drilling activity on their most productive prospects.

US oil imports are increasing in tandem with falling shale oil production and rising demand. We still have 260 million cars, trucks and buses that require mainly petroleum-based fuels, while electric vehicles make up a tiny fraction of the US vehicle fleet. If shale oil drilling were further curtailed by new regulations, the shortfall would be made up from non-US sources and imports would grow even faster. The party that stands to gain the most from that is OPEC.

From what I have seen and read, Secretary Clinton's proposed energy policy would undermine the all-of-the-above energy mix necessary to maintain US economic growth and energy security as we transition to cleaner energy sources. It is disconnected from the lessons of the last eight years and should not be implemented in its present form.

There is no doubt that Donald Trump views the shale revolution and the resources it has unlocked very differently from Secretary Clinton. It has been harder to gauge where he stands on other aspects of energy. During the primaries, Mr. Trump's energy policy lacked much detail, as I noted at the time. He has since largely remedied that, though many of the points raised on the energy page of his campaign's website seem mainly intended to counter Secretary Clinton's positions.

Mr. Trump's energy vision and goals are posted on his website, and he has made several speeches on the subject, focused mainly on expanding US oil and gas production and making the US a dominant global player in the markets for these commodities. His main theme is sweeping deregulation and reform, including revoking the current administration's executive orders and regulations affecting infrastructure projects, resource development, and the role of coal in power generation.

He endorses an all-of-the-above approach, but there's still little mention of renewables, efficiency or nuclear power. In any case his support for renewables is not linked to man-made climate change, which he disputes. He is also on record opposing US adherence to the Paris Climate Agreement.

How do Mr. Trump's ideas on energy square with the lessons of the last eight years? It seems clear he would rather swim with, rather than against the tide of the shale revolution. It's less clear how much additional activity that would stimulate in the near term if oil and gas prices remain low, even if regulations could be cut as he proposes. As for renewable energy, there doesn't seem to be enough information to assess where it fits into his version of "all of the above".

It's important to keep in mind that energy is not an end in itself. Stepping back from the details, and at the risk of grossly oversimplifying some complex and thorny issues, the key difference I see between the two candidates in this area is that Mrs. Clinton's energy policies seem designed mainly to serve environmental goals, while Mr. Trump's energy policies seem aimed at mainly economic goals.

In that sense, the choice here looks as binary as on many other issues this year. Just don't interpret that conclusion or my analysis above as an endorsement of either candidate.

As we look back, please recall that for most of the 2008 campaign the average US price for unleaded regular gasoline was over $3.00 per gallon. Much of that summer it was at or above $4.00. Four years later, from Labor Day to Election Day of 2012, regular gasoline averaged $3.76 per gallon. The comparable figure for the last two months of the 2016 campaign is just under $2.25.

In 2008 energy independence was a hot issue. Then-Senator Obama ran on a platform that targeted reducing US oil imports by over 3 million barrels per day, mainly through improved fuel efficiency. In his view US oil resources were effectively tapped out--remember "3% of reserves and 25% of consumption"? The main role he envisioned for the US oil and gas industry was as a source of increased tax revenue. His primary focus was on reducing greenhouse gas emissions through large federal investments in green energy technology. He would soon deliver on that promise with the $31 billion renewable energy package included in the federal stimulus of 2009.

When he was running for reelection in 2012, President Obama had kinder words for conventional energy, particularly the large expansion of US natural gas supply due to shale gas. He even took credit for "boosting US domestic production of oil". That point provoked an extended argument in the second presidential debate that year. Importantly, when the President emphasized renewable energy, energy efficiency and emissions, it was within a broader framework of "all of the above" energy.

At the same time, following the failure of comprehensive energy and climate legislation in his first term, his administration has pursued major new regulations aimed at achieving its energy and environmental goals. However, some of the most sweeping of these, including the Clean Power Plan, have gotten hung up in the courts, while others have yet to be fully implemented.

In retrospect President Obama was lucky. The shale energy revolution wasn't on his radar in 2008 and received little or no help from his administration, but it has increased US energy production by more than 17%, net of coal's losses, since he took office. It has made a major dent in US oil imports and CO2 emissions. In the process, it saved consumers hundreds of billions of dollars on their energy bills, reduced the US trade imbalance, generated large numbers of new jobs when it mattered most, and provided the primary means for reducing US greenhouse gas emissions to their lowest level since before Bill Clinton ran for President.

Meanwhile, the renewable energy revolution on which his 2008 campaign pinned most of its hopes is still a work in progress. The cost of non-hydro renewables, mainly wind and solar power, has fallen dramatically and their deployment has grown impressively, expanding by a combined 135% from 2008 to 2014, or 15% per year. Wind and solar power are reshaping US electricity markets and changing the economics of baseload power plants, including nuclear plants. However, these sources still generate just 8% of US electricity and accounted for less than 3% of total US energy production in 2015.

What can we learn from the experience of the last two presidential terms? We are certainly in the midst of a long-term transition from a high-carbon energy economy to one using lower-carbon fuels and low- or effectively zero-carbon electricity. However, the numbers tell us that with regard to implementation, if not technology, we are closer to the beginning of that transition than to its end. The next President can double renewables, and that would still leave us reliant on conventional energy and nuclear power for three-quarters of our electricity and 90% of our total energy needs.

Going from 3% of energy from new renewables to the levels needed to meet the emissions targets that the US took on at Paris last year represents an enormous technical and financial challenge. It won't happen without a healthy economy, supported by a diverse and flexible energy mix anchored by domestic oil and natural gas from public and private lands and waters.

Although the Obama administration has added numerous regulations affecting energy, it stopped short of derailing the shale revolution. As a result, it has benefited greatly from the increased flexibility and energy security shale is providing. President Obama adapted his approach to energy and came around to recognizing the need for an energy mix that balances new, green energy with the best conventional energy sources. That's the lens through which we should view the energy proposals of this year's candidates.

There's no question that Secretary Clinton would promote the continued growth of renewable energy and the wider application of energy efficiency. If anything, she seems to be even more focused on climate change and clean energy than Barrack Obama was in 2008. However, her campaign website portrays oil and gas mainly in negative terms, with a focus on cutting their consumption, along with the industry's tax benefits. While explicitly recognizing the role that increased US natural gas production has played in reducing emissions, her policies would directly target the primary source of that growth.

Shale gas now accounts for half of all US natural gas production, but Secretary Clinton is on record supporting much stricter regulations on "fracking", the common shorthand for the technological processes involved in producing oil and gas from shale: "By the time we get through all of my conditions, I do not think there will be many places in America where fracking will continue to take place,” she said in a March debate with Senator Sanders.

Reversing the recent growth of natural gas production from shale would lead to higher emissions during the next four to eight years. With less gas available, natural gas prices would rise, and the remaining coal-fired power plants would ramp back up to fill the gap, even as renewables continued to expand. That is happening in Germany today as that country turns away from nuclear power. In the US, without the contribution from natural gas and nuclear power plants, another of which just shut down permanently, our climate goals would be out of reach.

If implemented as described, Secretary Clinton's policy toward shale energy would have an even more pronounced effect on US energy supplies than restricting development on federal land. With oil prices low, shale oil production has already fallen by 1.2 million barrels per day since output peaked in May 2015. The drop would have been much steeper had US producers not been able to focus their greatly reduced drilling activity on their most productive prospects.

US oil imports are increasing in tandem with falling shale oil production and rising demand. We still have 260 million cars, trucks and buses that require mainly petroleum-based fuels, while electric vehicles make up a tiny fraction of the US vehicle fleet. If shale oil drilling were further curtailed by new regulations, the shortfall would be made up from non-US sources and imports would grow even faster. The party that stands to gain the most from that is OPEC.

From what I have seen and read, Secretary Clinton's proposed energy policy would undermine the all-of-the-above energy mix necessary to maintain US economic growth and energy security as we transition to cleaner energy sources. It is disconnected from the lessons of the last eight years and should not be implemented in its present form.

There is no doubt that Donald Trump views the shale revolution and the resources it has unlocked very differently from Secretary Clinton. It has been harder to gauge where he stands on other aspects of energy. During the primaries, Mr. Trump's energy policy lacked much detail, as I noted at the time. He has since largely remedied that, though many of the points raised on the energy page of his campaign's website seem mainly intended to counter Secretary Clinton's positions.

Mr. Trump's energy vision and goals are posted on his website, and he has made several speeches on the subject, focused mainly on expanding US oil and gas production and making the US a dominant global player in the markets for these commodities. His main theme is sweeping deregulation and reform, including revoking the current administration's executive orders and regulations affecting infrastructure projects, resource development, and the role of coal in power generation.

He endorses an all-of-the-above approach, but there's still little mention of renewables, efficiency or nuclear power. In any case his support for renewables is not linked to man-made climate change, which he disputes. He is also on record opposing US adherence to the Paris Climate Agreement.

How do Mr. Trump's ideas on energy square with the lessons of the last eight years? It seems clear he would rather swim with, rather than against the tide of the shale revolution. It's less clear how much additional activity that would stimulate in the near term if oil and gas prices remain low, even if regulations could be cut as he proposes. As for renewable energy, there doesn't seem to be enough information to assess where it fits into his version of "all of the above".

It's important to keep in mind that energy is not an end in itself. Stepping back from the details, and at the risk of grossly oversimplifying some complex and thorny issues, the key difference I see between the two candidates in this area is that Mrs. Clinton's energy policies seem designed mainly to serve environmental goals, while Mr. Trump's energy policies seem aimed at mainly economic goals.

In that sense, the choice here looks as binary as on many other issues this year. Just don't interpret that conclusion or my analysis above as an endorsement of either candidate.

Thursday, May 26, 2016

On Track for a Golden Age of Gas?

- The global energy industry must overcome significant new challenges if natural gas development is to achieve the vision of a Golden Age of Gas.

- Low energy prices and reduced investment are only half the battle as regulations complexify and organized opposition grows.

Five years ago the International Energy Agency (IEA) issued a report entitled, "Are We Entering a Golden Age of Gas?" Gas development was booming, from both conventional resources and US shale deposits, and gas was widely seen as a vital tool for reducing greenhouse gas emissions. Much has happened since then, including a collapse in global oil prices, the signing of a new climate agreement in Paris, and a broadening of the anti-fossil-fuel focus of climate activists. If we're still on the path to a golden age of gas, the ride will be bumpy.

This is probably most evident across the pond, where Nick Butler, the Financial Times' respected energy analyst, observed this week, "Unless something changes radically, Europe has passed the point of peak gas consumption." He cited Germany's ongoing "Energiewende" (energy transition) which in order to maximize wind and solar and minimize nuclear power, ends up squeezing gas out between renewables and much higher-emitting coal.

Earlier this month France's Energy Minister announced she was pursuing a ban on imports of US shale gas--effectively any gas from the US--since France already bans domestic fracking. That strikes me as a textbook example of having to keep making bad decisions to be consistent with the first one, but it's their sovereign choice.

As the IEA defined it at the time, this Golden Age would entail faster growth in gas demand in every major sector, compared to the agency's main "New Policies" scenario in its then-current annual World Energy Outlook (WEO). They anticipated compound average growth of 1.8% per year, much faster than oil or coal, with gas consumption ending up 13% higher than the WEO's projection for 2035. That's like adding an extra Russia or Middle East to world gas demand within 20 years.

One gauge of whether that still seems realistic can be found in the US Energy Information Administration's (EIA) just-released 2016 International Energy Outlook. The EIA's long-term forecast actually has gas consumption growing slightly faster than IEA's Golden Age track in the developed countries of the OECD between now and 2035, but with a slower ramp-up to essentially the same end-point in the non-OECD countries.

Of course one forecast can't really validate another, so let's consider how some of the big uncertainties that the IEA identified in the 2011 report have shifted, starting with energy pricing. After oil's recent rebound, oil and gas have fallen by around half their 2011 US prices. That makes investments in oil and gas exploration and production considerably less attractive. Nearly $400 billion of projects have been canceled or deferred, globally, setting up slower growth in production from both gas fields and oil fields with associated gas in the near-to-medium term. This deceleration is evident in EIA's latest monthly Drilling Productivity Report for US shale.

With the contract price of liquefied natural gas (LNG) often tied to oil prices or competing with pipeline gas that has also fallen in price, large gas infrastructure projects like LNG plants look less attractive, too. We've already seen cancellations of new facilities in Australia and Canada. Fewer LNG export facilities are likely to be built in the US than previously planned. All this means less new gas reaching markets where it can be used.

Cheaper oil also reduces the attractiveness of gas as a transportation fuel. Although increasingly popular as a cleaner fuel for buses, natural gas hasn't made much headway in US passenger cars. However, this application has been growing in places like Italy and Iran, for different reasons.

Viewed in isolation, these price-related responses seem likelier to delay, rather than derail the expectations the IEA set out in 2011. The bigger challenges come from a set of issues the IEA identified a year later, in a follow-up report called "Golden Rules for a Golden Age of Gas." As Dr. Birol, now the Executive Director of IEA, indicated then, these boil down to the industry's "social license to operate."

Transparency, water consumption, emissions including methane leaks--all on IEA's list--are some of the key issues over which companies, regulators, NGOs and activists are sparring today. The UK is a prime example. Conventional energy production is declining rapidly and a large shale gas potential has been identified by the British Geological Survey, but every attempt to drill exploratory wells has encountered strong opposition.

A new factor the IEA did not anticipate is the emergence of political movements focused on fossil fuel divestiture and a "keep it in the ground" mantra. These may be based on unrealistic expectations of how quickly the world can transition to a zero-emission economy, but they illustrate the scale of a stakeholder engagement challenge the global oil and gas industry has so far failed to meet adequately.

Just as social media are transforming politics, they are also altering the balance of power between organizations and their critics. The gaps that must be bridged if new gas development is to remain broadly acceptable to the public are growing in ways that will demand new approaches and new strategies to address.

Considering the shifts in the global energy mix that will be necessary to reduce global emissions in line with the goals of last year's Paris Agreement, gas ought to have a future every bit as bright as the Golden Age the IEA described five years ago. Achieving that now likely depends less on the price of energy and the scale of available resource than on convincing regulators and the public that the trade-offs involved in obtaining its benefits are still reasonable.

Wednesday, April 20, 2016

Out of Reach Without Nuclear and Shale

- US emissions reduction goals for 2025 could not be achieved without nuclear power and the fracking technology necessary to extract shale gas.

- Recent revisions by the EPA in its estimates of methane leaks from natural gas production and use do not negate the benefits of gas in reducing emissions.

The pie chart below shows the current sources of US electricity in terms of the energy they generate, rather than their rated capacity. This is an important distinction, because the renewable electricity technologies that have been growing so rapidly--wind and solar--are variable and/or cyclical, generating only a fraction of their rated output over the course of any week, month, or year.

For example, replacing the output of a 2,000 megawatt (MW) nuclear power plant such as the Indian Point facility just north of New York City would require, not 2,000 MW of wind and solar power, but between 7,600 MW and 9,400 MW, based on the applicable capacity factors for such installations. Now scale that up to the whole country. With 99 nuclear reactors in operation, rated at a combined 98,700 MW, it would take at least 375,000 MW of new wind and solar power to displace them. As the Post's editorial points out, money spent replacing already zero-emission energy is money not spent replacing high-emitting sources.

At the rates at which wind and solar capacity were added last year, that build-out would require 24 years. That's in addition to the 36 years it would take to replace the current contribution of coal-fired power generation. It also ignores the fact that intermittent renewables require either expensive energy storage or fast-reacting backup generation to provide 24/7 reliability.

That brings us to natural gas, the main provider of back-up power for renewables, and the "fracking" (hydraulic fracturing) technology that accounts for half of US natural gas production. Fracking has transformed the US energy industry so dramatically that it is very hard to gauge the consequences of a national ban on it, even if such a policy could be enacted. Would natural gas production fall by a third to its level in 2005, when shale gas made up only around 5% of US supply, and would imports of LNG and pipeline gas from Canada ramp back up, correspondingly?

Or would production fall even farther? After all, one of the main factors behind the rapid growth of shale gas in the previous decade is that US conventional gas opportunities in places like the Gulf of Mexico were becoming scarcer and more expensive to develop than shale, which was higher-cost then than today. Either way, the constrained supply of affordable natural gas under a fracking ban would not support generating a third of US electricity from gas, vs. 20% in 2006. So we would either need even more renewables and storage--in addition to those displacing nuclear power--or, as Germany has found in pursuit of its phase-out of nuclear power, a substantial contribution from coal.

One of the primary reasons cited by Mr. Sanders and others for their opposition to shale gas, aside from overstated claims about water impacts, is the risk to the climate from associated methane leaks. Here he would seem to have some support from the US Environmental Protection Agency, which recently raised its estimates of methane leakage from natural gas systems.

Methane is a much more powerful greenhouse gas than carbon dioxide (CO2), so this is a source of serious concern. However, a detailed look at the updated EPA data does not support the contention of shale's critics that natural gas is ultimately as bad or worse for the climate than coal, a notion that has been strongly refuted by other studies.

The oil and gas industry has questioned the basis of the EPA's revisions, but for purposes of discussion let's assume that their new figures are more accurate than last year's EPA estimate, which showed US methane emissions from natural gas systems having fallen by 11% since 2005. On the new basis, the EPA estimates that in 2014 gas-related methane emissions were 20 million CO2-equivalent metric tons higher than their 2013 level on the old basis, for a year-on-year increase of more than 12%. This upward revision is nearly offset by the 15 million ton drop in methane emissions from coal mining since 2009, which was largely attributable to gas displacing coal in power generation.

In any case, the new data shows gas-related emissions essentially unchanged since 2005, despite the 44% increase in US natural gas production over that period. The key comparison is that the EPA's entire, updated estimate of methane emissions from natural gas in 2014, on a CO2-equivalent basis, is just 2.5% of total US greenhouse gas emission that year. In particular, it equates to less than half of the 360 million ton per year reduction in emissions from fossil fuel combustion in electric power generation since 2005--a reduction well over half of which the US Energy Information Administration attributed to the shift from gas to coal.

In other words, from the perspective of the greenhouse gas emissions of the entire US economy, our increased reliance on natural gas for power generation cannot be making matters worse, rather than better. That's a good thing, because as I've shown above, we simply can't install enough renewables, fast enough, to replace coal, nuclear power and shale gas at the same time.

What does all this tell us? Fundamentally, Mr. Sanders and others advocating that the US abandon both nuclear power and shale gas are mistaken or misinformed. We are many years away from being able to rely entirely on renewable energy sources and energy efficiency to run our economy. In the meantime, nuclear and shale are essential for the continuing decarbonization of US electricity, which is the linchpin of the plans behind the administration's pledge at last December's Paris Climate Conference to reduce US greenhouse gas emissions by 26-28% by 2025. That goal would be out of reach without them.

Wednesday, January 27, 2016

2015: A Turning Point for Energy?

- 2015 was certainly an eventful year in energy, with plummeting oil prices and a widely anticipated global climate conference in December. It's less clear that it was a turning point.

When I sifted through the major energy developments of 2015, I was surprised by the number of references I found to last year as a turning point, whether for the oil industry, the response to climate change, coal-fired electricity generation, or renewable energy. To this list I am tempted to add the decision to allow unrestricted exports of US crude oil for the first time in 40 years.

Major turning points are best identified with the passage of time. With so many legitimate candidates it might seem a bit deflating to note, as the chart below reflects, that the growth pattern for US energy supplies in 2015 looks a lot like the one for 2014. Despite low prices, oil and gas output posted solid gains, at least through October, while wind and solar power contributed modestly, when compared on an energy-equivalent basis.

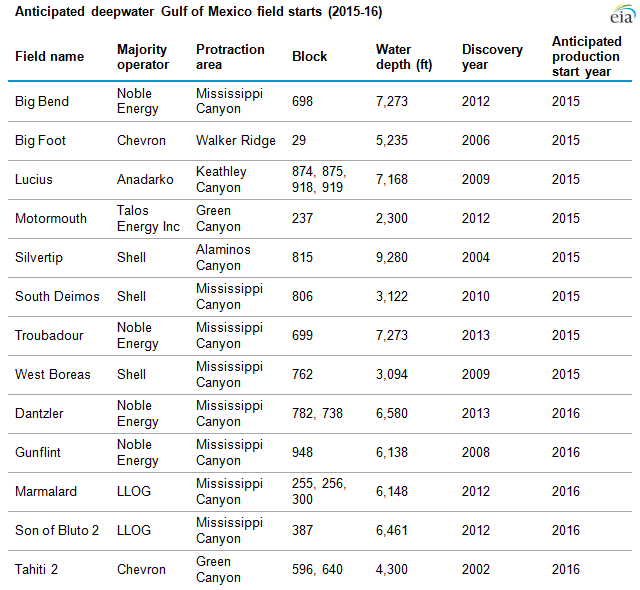

There are sound reasons to think that next year's graph may look quite different, starting with oil. The petroleum industry is still in turmoil from its turning point in late 2014, when OPEC declined to cut its output quota to restore the global oil market to balance. In North America and much of the world, drilling and investment in new projects are down sharply, and US oil production is retreating from the 44-year peak it reached in April. The subsequent decline would have been even more pronounced without the contribution of new deepwater platforms in the Gulf of Mexico that were planned long before oil prices fell.

Major turning points are best identified with the passage of time. With so many legitimate candidates it might seem a bit deflating to note, as the chart below reflects, that the growth pattern for US energy supplies in 2015 looks a lot like the one for 2014. Despite low prices, oil and gas output posted solid gains, at least through October, while wind and solar power contributed modestly, when compared on an energy-equivalent basis.

There are sound reasons to think that next year's graph may look quite different, starting with oil. The petroleum industry is still in turmoil from its turning point in late 2014, when OPEC declined to cut its output quota to restore the global oil market to balance. In North America and much of the world, drilling and investment in new projects are down sharply, and US oil production is retreating from the 44-year peak it reached in April. The subsequent decline would have been even more pronounced without the contribution of new deepwater platforms in the Gulf of Mexico that were planned long before oil prices fell.

{kind=link}

However, anyone identifying 2015 as the start of a global shift away from oil, rather than another cyclical low point, must contend with some contrary statistics. Global oil demand appears to have increased by around 2%--equivalent to the output of Nigeria--in response to a 70% drop in oil prices. And despite a lot of media attention, electric vehicles--the leading contender to replace the internal-combustion cars that are the main users of refined oil--have yet to catch on with mainstream consumers.

Based on data from Hybridcars.com, US sales of battery-electric vehicles (EVs) grew slightly faster than the 6% pace of the entire US car market in 2015 but still accounted for less than 0.5% of all new cars. In fact, the combined US market share of hybrids, plug-in hybrids and battery EVs fell by 18%, compared to 2014, to below 3%. This is a respectable start for vehicle electrification, but it's not much different from the beachhead that hybrids alone occupied in 2009.

Although we might look back on this situation in a few years as a turning point, I believe that will depend on the condition of OPEC and the global oil industry, as well as the level of global oil consumption, when supply and demand come back into balance and today's high oil inventories are drawn down.

At the launch of API's latest State of American Energy report earlier this month I had the opportunity to ask Jack Gerard, the President and CEO of API, how he thought the current situation might change the oil and gas industry, and whether it would push it even farther towards shale development, including outside the US. His response focused on ensuring that policies will allow US producers to compete globally and build on the advantages of US resources, capital markets and rule of law to increase their share of the market.

As for US natural gas production, rising per-well productivity and growth in the Utica shale and Permian Basin offset less drilling in general and output declines in the Marcellus shale and elsewhere. The continued expansion of gas is remarkable, considering that natural gas futures prices (front month) averaged just $ 2.63 per million BTUs for the year and dipped below $2 in December. The LNG exports set to begin this month look very timely.

Renewable energy, mainly in the form of wind and solar power, continues to grow rapidly as its costs decline. US renewables got an unexpected boost in December when the US Congress extended the two main federal tax credits for wind, solar and other technologies, including retroactively reinstating the lapsed wind Production Tax Credit (PTC). Renewables should also benefit from the implementation of the EPA's Clean Power Plan, and from the effect of the Paris climate agreement on the investment climate for these technologies.

We may not know for years whether the Paris Agreement was truly a turning point for climate change, as many have suggested. Another prescriptive agreement with legally binding targets, along the lines of the Kyoto Protocol, was never in the cards. However, the Paris text is replete with tentative verbs, along the lines of, "requests, invites, recognizes, aims, takes note, encourages, welcomes, etc. " It remains up to the participating countries whether and how they fulfill their voluntary Intended Nationally Determined Contributions and financial commitments.

The Paris Agreement could turn out to be the necessary framework for firm steps by both developed and developing countries to reduce emissions and adapt to climatic changes that are already "baked in", or it might shortly be overtaken by other events, as previous climate change measures were in the aftermath of the 2008 financial crisis. The current financial problems of the world's largest emitter of greenhouse gases--arguably the most important signatory to the Paris Agreement--are not a positive signal.

With so many uncertainties in play, we should consider all of these potential turning points as signposts of changes that depend on other interconnected factors, if they are to lead to a future that breaks with the status quo. There are enough of them to make for a very interesting 2016, even if this wasn't also a US presidential election year.

A different version of this posting was previously published on the website of Pacific Energy Development Corporation.

Wednesday, December 16, 2015

A Grand Compromise on Energy?

The idea of a Congressional "grand compromise" on energy has been debated for years. A decade ago, such an agreement might have opened up access for drilling in the Arctic National Wildlife Refuge, in exchange for "cap and trade" or some other comprehensive national greenhouse gas emissions policy. By comparison, the deal apparently included in the 2016 spending and tax bill is small beer but still worthwhile: In exchange for lifting the outdated restrictions on exporting US crude oil, Congress will respectively revive and extend tax credits for wind and solar power.

Anticipation about the prospect of US oil exports seemed higher last year, when production was growing rapidly and threatening to outgrow the capacity of US oil refineries to handle the volumes of high-quality "tight oil" flowing from shale deposits. Just this week Michael Levi of the Council on Foreign Relations, citing a study by the Energy Information Administration, suggested that allowing such exports might now be nearly inconsequential in most respects.

Although little additional oil may flow in the short term, given the current global surplus, it's worth recalling that the gap between domestic and international oil prices hasn't always been as narrow as it is today. The discount for West Texas Intermediate relative to UK Brent crude has averaged around $4 per barrel this year, but within the last three years it has been as wide as $15-20. Oil traders will tell you that average differentials between markets are essentially irrelevant. What counts is the windows when those gaps widen, during which a lot of cargoes can move in short periods.

No matter how much or little US oil is ultimately exported, and how much additional production the lifting of the export ban will actually stimulate, the bigger impact on the global oil market is likely to be psychological. Having to find new outlets for oil shipped from West Africa, for example, because US refiners are processing more US crude and importing less from elsewhere is one thing; having to compete directly with cargoes of US oil is going to be quite another. That's where US consumers will benefit in the long run, from lower global oil prices that translate into lower prices at the gas pump.

Finally, if OPEC can choose to cease acting like a cartel--at least for the moment--and treat crude oil as a normal market, then it's timely for the US to follow suit and end an oil export ban that originated in the same 1970s oil crisis that put OPEC on the map.

How about the other side of this deal? What do we get for retroactively reinstating the expired wind production tax credit (PTC), along with extending the 30% solar tax credit that would have expired at the end of next year?

We'll certainly get more wind farms, along with some stability for an industry that has been whipsawed by past expirations and last-minute extensions of a tax credit that has been a major driver of new installations throughout its 20+ year history. Wind energy accounted for 4.4% of US grid electricity in the 12 months through September, up from a little over 1% in 2008.

However, this tax credit isn't cheap . The 4,800 Megawatts of new wind turbines installed in 2014 will receive a total of nearly $2.5 billion in subsidies--equivalent to around $19 per barrel--during the 10 years in which they will be eligible for the PTC, and 2015's additions are on track to beat that. The PTC is also the policy that enables wind power producers in places like Texas to sell electricity at prices below zero--still pocketing the 2.3¢ per kilowatt-hour (kWh) tax credit--distorting wholesale electricity markets and capacity planning.

As for solar power, it's not obvious that the tax credit extension was necessary at all, in light of the rapid decline in the cost of solar photovoltaic energy (PV). In any case, because the tax credit for solar is calculated as a percentage of installed cost, rather than a fixed subsidy per kWh of output like for wind, the technology's progress has provided an inherent phaseout of the dollar benefit. Solar's rapid growth seems likely to continue, with or without the tax credit.

The big missed opportunity from a clean energy and climate perspective is that these tax credit extensions channel billions of dollars to technologies that, at least in the case of wind, are essentially mature and widely regarded as inadequate to support a large-scale, long-term transition to low-emission energy. I would have preferred to see these federal dollars targeted to help incubate new energy technologies, along the lines of the Breakthrough Energy Coalition announced by Bill Gates and other high-tech leaders at the Paris climate conference.

The current deal, embedded within a $1.6 trillion "omnibus" spending bill, must still pass the Congress and be signed by the President. It won't please everyone, but it is at least consistent with the "all of the above" approach that has been our de facto energy strategy, at least since 2012. It also serves as a reminder that despite the commitments at Paris to reduce emissions of CO2 and other greenhouse gases, renewable energy will of necessity coexist with oil and gas for many years to come.

Anticipation about the prospect of US oil exports seemed higher last year, when production was growing rapidly and threatening to outgrow the capacity of US oil refineries to handle the volumes of high-quality "tight oil" flowing from shale deposits. Just this week Michael Levi of the Council on Foreign Relations, citing a study by the Energy Information Administration, suggested that allowing such exports might now be nearly inconsequential in most respects.

Although little additional oil may flow in the short term, given the current global surplus, it's worth recalling that the gap between domestic and international oil prices hasn't always been as narrow as it is today. The discount for West Texas Intermediate relative to UK Brent crude has averaged around $4 per barrel this year, but within the last three years it has been as wide as $15-20. Oil traders will tell you that average differentials between markets are essentially irrelevant. What counts is the windows when those gaps widen, during which a lot of cargoes can move in short periods.

No matter how much or little US oil is ultimately exported, and how much additional production the lifting of the export ban will actually stimulate, the bigger impact on the global oil market is likely to be psychological. Having to find new outlets for oil shipped from West Africa, for example, because US refiners are processing more US crude and importing less from elsewhere is one thing; having to compete directly with cargoes of US oil is going to be quite another. That's where US consumers will benefit in the long run, from lower global oil prices that translate into lower prices at the gas pump.

Finally, if OPEC can choose to cease acting like a cartel--at least for the moment--and treat crude oil as a normal market, then it's timely for the US to follow suit and end an oil export ban that originated in the same 1970s oil crisis that put OPEC on the map.

How about the other side of this deal? What do we get for retroactively reinstating the expired wind production tax credit (PTC), along with extending the 30% solar tax credit that would have expired at the end of next year?

We'll certainly get more wind farms, along with some stability for an industry that has been whipsawed by past expirations and last-minute extensions of a tax credit that has been a major driver of new installations throughout its 20+ year history. Wind energy accounted for 4.4% of US grid electricity in the 12 months through September, up from a little over 1% in 2008.

However, this tax credit isn't cheap . The 4,800 Megawatts of new wind turbines installed in 2014 will receive a total of nearly $2.5 billion in subsidies--equivalent to around $19 per barrel--during the 10 years in which they will be eligible for the PTC, and 2015's additions are on track to beat that. The PTC is also the policy that enables wind power producers in places like Texas to sell electricity at prices below zero--still pocketing the 2.3¢ per kilowatt-hour (kWh) tax credit--distorting wholesale electricity markets and capacity planning.

As for solar power, it's not obvious that the tax credit extension was necessary at all, in light of the rapid decline in the cost of solar photovoltaic energy (PV). In any case, because the tax credit for solar is calculated as a percentage of installed cost, rather than a fixed subsidy per kWh of output like for wind, the technology's progress has provided an inherent phaseout of the dollar benefit. Solar's rapid growth seems likely to continue, with or without the tax credit.

The big missed opportunity from a clean energy and climate perspective is that these tax credit extensions channel billions of dollars to technologies that, at least in the case of wind, are essentially mature and widely regarded as inadequate to support a large-scale, long-term transition to low-emission energy. I would have preferred to see these federal dollars targeted to help incubate new energy technologies, along the lines of the Breakthrough Energy Coalition announced by Bill Gates and other high-tech leaders at the Paris climate conference.

The current deal, embedded within a $1.6 trillion "omnibus" spending bill, must still pass the Congress and be signed by the President. It won't please everyone, but it is at least consistent with the "all of the above" approach that has been our de facto energy strategy, at least since 2012. It also serves as a reminder that despite the commitments at Paris to reduce emissions of CO2 and other greenhouse gases, renewable energy will of necessity coexist with oil and gas for many years to come.

Tuesday, November 10, 2015

The Keystone Rejection and the Shift Back toward OPEC

Although the International Energy Agency's latest warning of future energy security risks doesn't mention the Keystone XL pipeline, it provides important context for assessing President Obama's decision turning down that project's application. The IEA's newly issued global energy forecast indicates that if oil prices remain low until the end of the decade, it "would trigger energy-security concerns by heightening reliance on a small number of low-cost producers," a polite way of referring to OPEC. The Keystone verdict could help reinforce that shift.

I've devoted a lot of posts to different aspects of the Keystone issue. In a post last year on the State Department's Final Supplemental Environmental Impact Statement, I pointed out the pipeline's relatively modest potential to affect climate change, with a range of incremental greenhouse gas emissions (GHGs) equating to 0.02-0.4% of total US emissions. Even if the full lifecycle emissions of the oil sands crude it would have transported were included, they would still not have exceed around 0.3% of global CO2-equivalent emissions. For these and other reasons, I have consistently concluded that the decision would be made on political, rather than technical grounds, consistent with the symbolism the project has taken on with environmental activists during this administration.

Whether the Keystone rejection is attributable mainly to domestic political considerations or to positioning in advance of next month's Paris climate conference is a minor distinction. As the editors of the Washington Post put it, the distortion and politicization of the issue "was a national embarrassment, reflecting poorly on the United States’ capability to treat parties equitably under law and regulation." If the IEA's assessment of the trends underlying today's low oil prices is correct, we may come to regret last Friday's ruling for other reasons, too.

Recall that last year's oil-price collapse had two principal triggers: surging US oil production from shale deposits in Texas, North Dakota and several other states, and a decision by OPEC to forgo its historic role as balancers of the global oil market and instead to produce full out. The latter explains why oil remains below $50 per barrel, even though US shale output is now retreating.

Yet while shale production is expected to rebound once prices start to recover--whenever that might occur--the same cannot necessarily be said for conventional non-OPEC production from places like the North Sea and other high-cost, mature regions. Oil companies have canceled or deferred over $200 billion in exploration and production projects, while existing oil fields accounting for more than 10 times the output of US shale will continue to decline at rates of perhaps 5-10% per year.

The combination of all these factors sets the stage for a future oil market very different from what we've experienced in the past few decades. If OPEC and particularly Saudi Arabia assume the role of baseload, rather than swing producers, the price of oil will be set by the last, most expensive barrels to be supplied. That would constitute a much more normal market than one that has been dominated by OPEC production quotas, but it would also lack the margin of 3-5 million barrels per day of "spare capacity" that OPEC has typically held in reserve. That is a recipe for increased risk and volatility ahead.

If this comes to pass, the result might not be an exact re-run of the oil crises of the 1970s. The global economy is much less reliant on oil than it was four decades ago, especially for electricity generation, which as the IEA points out will increasingly come from renewable sources. However, oil will remain indispensable for transportation for many years. In a global oil market again dominated by OPEC, additional pipeline-based supplies from a reliable neighbor like Canada would be highly desirable, and the US Strategic Petroleum Reserve, which the Congress just voted to shrink in order to raise a couple of billion dollars of revenue, could become a lot more valuable.

The decision to reject TransCanada's application for the Keystone XL pipeline was ostensibly made on long-term considerations related to climate change, but it reflects a short-sighted view of energy markets. In that light, the President's conclusion that Keystone "would not serve the national interests of the United States" seems very likely to be revisited by a future US president.

I've devoted a lot of posts to different aspects of the Keystone issue. In a post last year on the State Department's Final Supplemental Environmental Impact Statement, I pointed out the pipeline's relatively modest potential to affect climate change, with a range of incremental greenhouse gas emissions (GHGs) equating to 0.02-0.4% of total US emissions. Even if the full lifecycle emissions of the oil sands crude it would have transported were included, they would still not have exceed around 0.3% of global CO2-equivalent emissions. For these and other reasons, I have consistently concluded that the decision would be made on political, rather than technical grounds, consistent with the symbolism the project has taken on with environmental activists during this administration.

Whether the Keystone rejection is attributable mainly to domestic political considerations or to positioning in advance of next month's Paris climate conference is a minor distinction. As the editors of the Washington Post put it, the distortion and politicization of the issue "was a national embarrassment, reflecting poorly on the United States’ capability to treat parties equitably under law and regulation." If the IEA's assessment of the trends underlying today's low oil prices is correct, we may come to regret last Friday's ruling for other reasons, too.

Recall that last year's oil-price collapse had two principal triggers: surging US oil production from shale deposits in Texas, North Dakota and several other states, and a decision by OPEC to forgo its historic role as balancers of the global oil market and instead to produce full out. The latter explains why oil remains below $50 per barrel, even though US shale output is now retreating.

Yet while shale production is expected to rebound once prices start to recover--whenever that might occur--the same cannot necessarily be said for conventional non-OPEC production from places like the North Sea and other high-cost, mature regions. Oil companies have canceled or deferred over $200 billion in exploration and production projects, while existing oil fields accounting for more than 10 times the output of US shale will continue to decline at rates of perhaps 5-10% per year.

The combination of all these factors sets the stage for a future oil market very different from what we've experienced in the past few decades. If OPEC and particularly Saudi Arabia assume the role of baseload, rather than swing producers, the price of oil will be set by the last, most expensive barrels to be supplied. That would constitute a much more normal market than one that has been dominated by OPEC production quotas, but it would also lack the margin of 3-5 million barrels per day of "spare capacity" that OPEC has typically held in reserve. That is a recipe for increased risk and volatility ahead.

If this comes to pass, the result might not be an exact re-run of the oil crises of the 1970s. The global economy is much less reliant on oil than it was four decades ago, especially for electricity generation, which as the IEA points out will increasingly come from renewable sources. However, oil will remain indispensable for transportation for many years. In a global oil market again dominated by OPEC, additional pipeline-based supplies from a reliable neighbor like Canada would be highly desirable, and the US Strategic Petroleum Reserve, which the Congress just voted to shrink in order to raise a couple of billion dollars of revenue, could become a lot more valuable.

The decision to reject TransCanada's application for the Keystone XL pipeline was ostensibly made on long-term considerations related to climate change, but it reflects a short-sighted view of energy markets. In that light, the President's conclusion that Keystone "would not serve the national interests of the United States" seems very likely to be revisited by a future US president.

Monday, January 05, 2015

2014 in Review: Shale Energy's First Price Cycle

2014 was an extraordinary year in energy, vividly illustrating both sides of the Chinese proverb about interesting times. Oil market volatility was the big story for much of the year, with the dominance of geopolitical risks finally yielding to surging supplies. Of the two energy revolutions underway, shale wields the bigger stick for now, while the growth of renewables gathers momentum. All of this has implications for 2015 and beyond.

The US remained the epicenter of the shale revolution this year, with development elsewhere still subject to uncertainties about economic production potential, infrastructure, and the rules of the road. A comparison of oil-equivalent additions to US energy supplies from oil, gas and non-hydro renewables for the first nine months of the year highlights both the significance of shale and the differences in relative scale that impede a rapid shift to renewables.

|  |

US shale drilling added over a million barrels per day of "light tight oil" (LTO) production, compared to 2013, based on US Energy Information Administration data for the first nine months of the year. That brings cumulative gains since 2011 to nearly 3 million bbl/day. This hasn't just upended the global oil market; it has also revolutionized the way oil moves across North America. Over a million bbl/day now moves by rail, a figure recently projected to peak at 1.5 million by 2016. Nor is that entirely the result of delays to pipeline projects like Keystone XL. One proposed pipeline for Bakken LTO was reportedly canceled due to a lack of interest from shippers. Rail is expensive but provides producers and refiners with greater flexibility in both volume and destinations than fixed pipelines.

The collapse of oil prices has prompted many producers to reassess drilling plans, although it has been a boon for refiners and consumers. Refining margins look relatively healthy, at least based on the proxy of "crack spreads", the difference between the wholesale prices of gasoline and diesel and the oil from which they are made. Some refiners also anticipate that low prices will spur demand growth, as described in a fascinating Wall St. Journal interview with Tom O'Malley, who has turned a succession of castoff refineries into profitable businesses.

We may already be seeing the demand response to lower prices. November US volumes were at a 7-year high, according to API. This is unlikely to be replicated quickly elsewhere, however, for the same reasons that global oil demand was slow to moderate when prices rose over the last several years: In many countries the influence of oil prices on consumer behavior is overwhelmed by fuel taxes or subsidies. With prices now falling, some developing countries are capitalizing on the opportunity to unwind billions of dollars in consumption subsidies, offsetting market drops. That could have important implications for future oil demand and greenhouse gas emissions.

Meanwhile US consumers have watched retail gasoline prices fall by $1.39 per gallon since July and by over a dollar compared to a year ago. If sustained, the effective stimulus could exceed $100 billion annually, ignoring the effect of lower prices for jet fuel, diesel and other products. It's not surprising that half of respondents in last month's Wall St. Journal/NBC poll indicated this was important for their families.

While oil has been making headlines, shale gas without much fanfare added the equivalent of another half-million bbl/day to US production. That explains why despite enormous drawdowns of gas during last winter's "Polar Vortex", gas inventories began this winter much closer to normal levels than was widely expected in the spring. Gas has lost a little ground in electricity generation to coal in the last two years, but few reading the EPA's proposed Clean Power Plan regulation would expect that trend to continue.

Shale gas remains controversial in some areas due to perceived environmental and community impacts. New York state is apparently making its temporary ban on hydraulic fracturing ("fracking") permanent, preferring to rely on shale gas supplies from neighboring Pennsylvania. Yet while shale drilling in North Dakota has led to an increase in gas flaring--burning off gas that can't economically reach a market--the latest findings from the University of Texas and Environmental Defense Fund measured methane leakage from gas wells at an average of 0.43%. That shrinks gas's emissions footprint and enhances its potential role in climate change mitigation.

Turning to renewables, wind energy now provides a little over 4% of US electricity. However, its growth has slowed due to uncertainty about continued federal subsidies. The wind production tax credit, or PTC, had previously been extended through 2013 in a way that allowed projects brought online later to benefit from the extension. It was just extended again through the end of 2014, along with a broad package of other expiring tax benefits. This late revival might be a gift to a few projects already under construction, but it seems unlikely to spur additional projects without further legislative action in the new Congress.