- The data analysis arm of the US Department of Energy is forecasting that despite low oil prices, the US will become energy independent within a decade.

- That result depends on frugality as much as resource abundance, and it includes substantial volumes of energy trade with the rest of the world.

The US Energy Information Administration's latest Annual Energy Outlook features the key finding that the US is on track to reduce its net energy imports to essentially zero by 2030, if not sooner. That might seem surprising, in light of the recent collapse of oil prices and the resulting significant slowdown in drilling. EIA has covered that base, as well, in a side-case in which oil prices remain under $80 per barrel through 2040, and net imports bottom out at around 5% of total energy demand. Either way, this is as close to true US energy independence as I ever expected to see.

|

It wasn't that many years ago that such an outcome seemed ludicrously unattainable. I recall patiently explaining to various audiences that we simply couldn't drill our way to energy independence. The forecast of self-sufficiency that EIA has assembled depends on a lot more than just drilling, but without the development of previously inaccessible oil and gas resources through advanced drilling technology and hydraulic fracturing, a.k.a. "fracking", it couldn't be made at all. The growing contributions of various renewables are still dwarfed by oil and natural gas, for now.

Every forecast depends on assumptions, and it's important to understand what would be necessary in order for conditions to turn out as the EIA now expects in its "reference case", or main scenario. This includes a gradual but pronounced oil-price recovery, to average just over $70/bbl next year, $80 within five years, and back to around $100 by the end of the 2020s. That helps support a resumption of oil production growth next year, followed by a plateau just above 10 million bbl/day--surpassing 1971's peak output--for the next decade and a gradual decline thereafter. EIA also expects natural gas prices to head back towards $5 per million BTUs by the end of this decade, in tandem with a further 34% expansion of US gas production by 2040.

However, attainment of zero net imports also depends on the continuation of some important trends, including energy consumption that grows at a rate well below that of population, and a continued decoupling of energy and GDP growth. This is crucial, because through 2040 EIA assumes the US population will grow by another 20% and GDP by 85%, while total energy consumption increases by just 10%. That has important implications for greenhouse gas emissions, too. Energy-related emissions barely grow at all in this scenario.

Renewable energy output is also expected to continue growing, with US electricity generated from wind surpassing that from hydropower in the late 2030s and solar power in 2040 yielding roughly as many megawatt-hours as wind did in 2008.

Finally, reaching a balance between US energy imports and exports also depends on the continued contribution of nuclear power at roughly current levels. That suggests that new reactors in other locations will replace those that are retired, including for economic reasons.

In last month's rollout presentation at the Center for Strategic & International Studies (CSIS) in Washington, EIA Administrator Sieminski also emphasized what is not included in the Outlook's assumptions, notably the EPA's "Clean Power Plan" that is currently under review. It would be hard to imagine US coal consumption remaining essentially unchanged at 18% of the total energy mix in 2040, if EPA's plan to reduce emissions from the electricity sector by 30% by 2030 were fully implemented. EIA will apparently issue its analysis of the impact of the Clean Power Plan this month.

It's also worth comparing EIA's view of zero net energy imports with popular notions of what energy independence. It certainly does not mean that the US would no longer import any oil, natural gas, or other fuels from other countries. Even as the US approaches zero net imports, routine imports and exports of various energy streams will remain necessary to address imbalances between regions and fuel types.

Because EIA's forecast is predicated on current laws and regulations, it does not include any significant growth in oil exports. As a result, exports of refined products such as propane, gasoline and diesel fuel would continue to expand, eventually exceeding 6 million bbl/day gross and 4 million net of imports. In its "High Oil and Gas Resource" case the constraint on US oil exports forces an expansion of refined product exports that seems nearly incredible when refinery capacity in Asia and the Middle East is also slated for expansion, while refined product demand growth slows globally. Perhaps this is EIA's subtle way of focusing attention on the US's outdated oil export regulations.

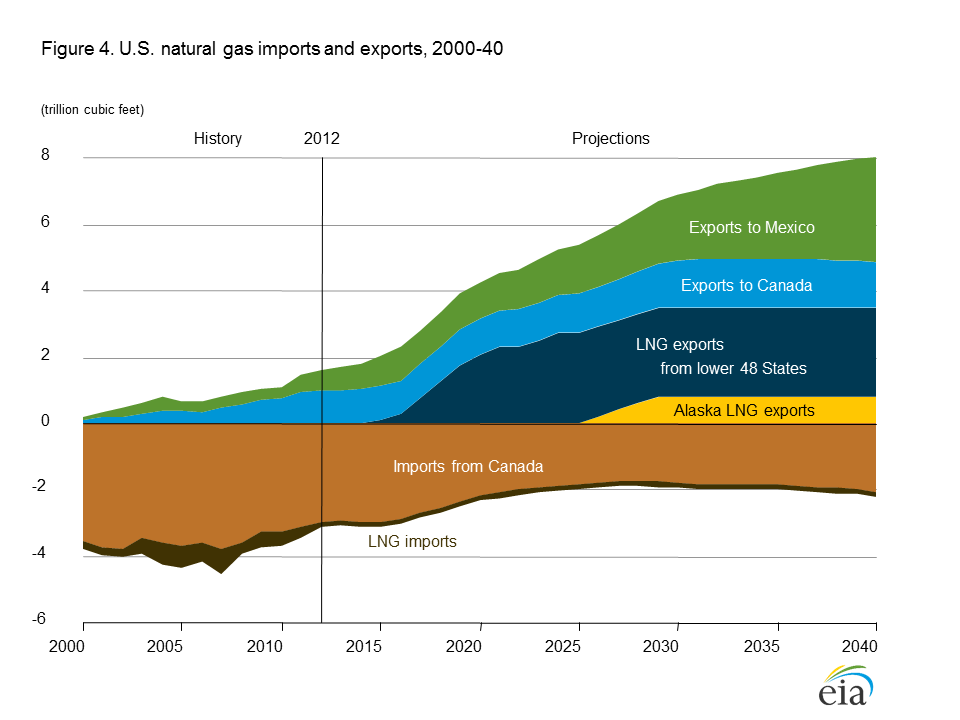

Exports of liquefied natural gas (LNG) would also take off, accounting for around 9% of US production by 2040, while imports of pipeline gas from Canada would shrink but not disappear. In the high resource case, US LNG exports would grow dramatically until the late 2030s, reaching 20% of a much bigger supply.

The report provides a few surprises, including one that won't be welcomed by advocates of biofuels and a continuation of the current federal Renewable Fuels Standard, the reform of which has gradually become a topic of lively debate in the US Congress. EIA's figures show total US biofuel consumption growing by less than 1% per year, with ethanol's only real growth coming in the form of a modest increase in sales of E85, a mixture of 85% ethanol and 15% gasoline, to around 3% of gasoline demand in 2040.

Overall, I'm struck by several things. First, the value of the EIA's forecasts comes mainly from identifying the implications of current trends and policies, rather than accurately predicting the future. Administrator Sieminski seemed appropriately humble about the latter task in his remarks at CSIS. Yet the reference case this time suggests an eventual reversion to pre-oil-crash conditions, ending in 2040 at the same oil price in 2013 dollars as last year's forecast--a level that would exceed the 2008 peak by a sizeable margin. That seems inconsistent with a world of expanding energy options, improved drilling efficiency, at least for shale, and a growing focus on the decarbonization of energy.

There also appears to be a disconnect between the forecast's rising real price of natural gas, with implications for the cost of electricity generation, and its virtual flatlining of solar power's expansion after the scheduled expiration of the current solar tax credit in 2016. This looks like a bet against further solar cost reductions and technology improvements, along with structural changes that are already occurring in some electricity markets.

Despite these reservations, I wouldn't dispute the headline finding of steady progress toward a version of US energy independence featuring large volumes of energy trade with both North America and the rest of the world. The combination of resource growth and steady energy efficiency improvements looks like a recipe for finally putting the US on an energy footing that politicians of both major parties have only dreamed of for the last 40 years.

Every forecast depends on assumptions, and it's important to understand what would be necessary in order for conditions to turn out as the EIA now expects in its "reference case", or main scenario. This includes a gradual but pronounced oil-price recovery, to average just over $70/bbl next year, $80 within five years, and back to around $100 by the end of the 2020s. That helps support a resumption of oil production growth next year, followed by a plateau just above 10 million bbl/day--surpassing 1971's peak output--for the next decade and a gradual decline thereafter. EIA also expects natural gas prices to head back towards $5 per million BTUs by the end of this decade, in tandem with a further 34% expansion of US gas production by 2040.

However, attainment of zero net imports also depends on the continuation of some important trends, including energy consumption that grows at a rate well below that of population, and a continued decoupling of energy and GDP growth. This is crucial, because through 2040 EIA assumes the US population will grow by another 20% and GDP by 85%, while total energy consumption increases by just 10%. That has important implications for greenhouse gas emissions, too. Energy-related emissions barely grow at all in this scenario.

Renewable energy output is also expected to continue growing, with US electricity generated from wind surpassing that from hydropower in the late 2030s and solar power in 2040 yielding roughly as many megawatt-hours as wind did in 2008.

Finally, reaching a balance between US energy imports and exports also depends on the continued contribution of nuclear power at roughly current levels. That suggests that new reactors in other locations will replace those that are retired, including for economic reasons.

In last month's rollout presentation at the Center for Strategic & International Studies (CSIS) in Washington, EIA Administrator Sieminski also emphasized what is not included in the Outlook's assumptions, notably the EPA's "Clean Power Plan" that is currently under review. It would be hard to imagine US coal consumption remaining essentially unchanged at 18% of the total energy mix in 2040, if EPA's plan to reduce emissions from the electricity sector by 30% by 2030 were fully implemented. EIA will apparently issue its analysis of the impact of the Clean Power Plan this month.

It's also worth comparing EIA's view of zero net energy imports with popular notions of what energy independence. It certainly does not mean that the US would no longer import any oil, natural gas, or other fuels from other countries. Even as the US approaches zero net imports, routine imports and exports of various energy streams will remain necessary to address imbalances between regions and fuel types.

Because EIA's forecast is predicated on current laws and regulations, it does not include any significant growth in oil exports. As a result, exports of refined products such as propane, gasoline and diesel fuel would continue to expand, eventually exceeding 6 million bbl/day gross and 4 million net of imports. In its "High Oil and Gas Resource" case the constraint on US oil exports forces an expansion of refined product exports that seems nearly incredible when refinery capacity in Asia and the Middle East is also slated for expansion, while refined product demand growth slows globally. Perhaps this is EIA's subtle way of focusing attention on the US's outdated oil export regulations.

Exports of liquefied natural gas (LNG) would also take off, accounting for around 9% of US production by 2040, while imports of pipeline gas from Canada would shrink but not disappear. In the high resource case, US LNG exports would grow dramatically until the late 2030s, reaching 20% of a much bigger supply.

The report provides a few surprises, including one that won't be welcomed by advocates of biofuels and a continuation of the current federal Renewable Fuels Standard, the reform of which has gradually become a topic of lively debate in the US Congress. EIA's figures show total US biofuel consumption growing by less than 1% per year, with ethanol's only real growth coming in the form of a modest increase in sales of E85, a mixture of 85% ethanol and 15% gasoline, to around 3% of gasoline demand in 2040.

Overall, I'm struck by several things. First, the value of the EIA's forecasts comes mainly from identifying the implications of current trends and policies, rather than accurately predicting the future. Administrator Sieminski seemed appropriately humble about the latter task in his remarks at CSIS. Yet the reference case this time suggests an eventual reversion to pre-oil-crash conditions, ending in 2040 at the same oil price in 2013 dollars as last year's forecast--a level that would exceed the 2008 peak by a sizeable margin. That seems inconsistent with a world of expanding energy options, improved drilling efficiency, at least for shale, and a growing focus on the decarbonization of energy.

There also appears to be a disconnect between the forecast's rising real price of natural gas, with implications for the cost of electricity generation, and its virtual flatlining of solar power's expansion after the scheduled expiration of the current solar tax credit in 2016. This looks like a bet against further solar cost reductions and technology improvements, along with structural changes that are already occurring in some electricity markets.

Despite these reservations, I wouldn't dispute the headline finding of steady progress toward a version of US energy independence featuring large volumes of energy trade with both North America and the rest of the world. The combination of resource growth and steady energy efficiency improvements looks like a recipe for finally putting the US on an energy footing that politicians of both major parties have only dreamed of for the last 40 years.

A different version of this posting was previously published on the website of Pacific Energy Development Corporation

{kind=link}

{kind=link}

{kind=link}

_in_thousand_terajoules_(GCV)-tb1.png&filetimestamp=20130625095947){kind=link}

{kind=link}