- China's decision on whether and when to ban cars burning gasoline and diesel could alter our view of how far we are from a peak in global oil demand.

- Even though the likely date of such a peak is highly uncertain, the idea of an impending peak could significantly affect investments and other decisions.

Now it appears that China is preparing to issue a similar ban. With around 30% of global new-vehicle sales, China could upend the plans and economics of the world's fuel and automobile industries. However, it is less obvious that this would lead directly to the arrival of "peak demand" for oil, an idea that has largely displaced earlier thoughts of Peak Oil related to supply.

Some background is in order, because the two concepts are easy to confuse. Peak Oil, which gained considerable traction with investors and the public in the 2000s, was based on the undoubted fact that the quantity of oil in the earth's crust is finite, at least on a human time-scale. Its proponents argued that we were nearing a geological limit on oil production, and that quite soon oil companies and OPEC nations wouldn't be able to sustain their current production, let alone continue adding to it every year.

The presumption that such a peak was imminent has been pretty clearly refuted by the shale revolution, the first stages of which had already begun when Peak Oil was still fashionable. In fact, humanity has only extracted a small percentage of the world's oil resources. We continue to find both additional resources and new ways to extract more from previously identified resources. Global proved oil reserves--a measure of how much can be produced economically with current technology--have more than doubled since 1980, while production (and consumption) grew by 34%.

For that matter, many of the shale plays that today produce a total of more than 4 million barrels per day had been known for decades. Petroleum engineers just didn't see how to produce oil from them in commercial volumes and at a cost that could compete with other sources like oil fields in deep water.

The first mention I heard of "peak demand" was at an IHS investment conference in 2009, when supply-focused Peak Oil was still king. At the time, it was a novel idea, since only a year earlier, oil prices crested just short of $150 per barrel on the back of surging demand and, to some extent the expectation of Peak Oil, and were only tamed by the unfolding global financial crisis.

Peak demand proposes that consumption of petroleum and its products will reach its maximum extent within a few decades, and thereafter plateau or fall. Crucially, it doesn't depend on a single theory, but on a combination of factors that are easily observable, though still uncertain in their future progression: meaningful improvements in fuel economy, even for large vehicles; policies and regulations to decarbonize the global energy system in response to climate change; an apparent decoupling of GDP and energy consumption; and the rise of partially and fully electrified vehicles.

That brings us back to the implications of a ban on internal combustion engine (ICE) cars in China. Considering that China has accounted for roughly a third of the increase in global oil consumption since 2014, this has to be reckoned as one of the larger uncertainties about future oil demand. Even if we're only talking about the equivalent of a couple of million barrels per day of lost demand growth by 2030, OPEC's ongoing struggle to balance a market that has been oversupplied by less than that amount puts the potential impact for oil investment and economics into sharp relief.

China has every incentive to take this step. Its urban air pollution is on a scale that cities like London and L.A. haven't experienced since the 1950s or 1960s. The country's 2015 pledge to limit greenhouse gas emissions was a centerpiece, and arguably the sine qua non, of the Paris climate agreement. If that weren't enough, the country's dependence on oil imports is exploding in much the same way as the US's did in the early-to-mid 2000s.

Perhaps I'm cynical to think that the last point weighs most heavily on China's policy-makers, just as US energy debates hinged on energy security concerns until quite recently. China's oil demand continues to grow, with over 20 million new cars and trucks reaching its roads each year, and the vast majority of them still needing gasoline or diesel fuel. Meanwhile, its oil production is going sideways, at best, as its mature oil fields decline.

Moreover, despite the country's large unconventional oil resource potential there does not seem to be a shale light at the end of their tunnel, because most of the conditions that supported the shale revolution here don't apply within China's state-dominated system. What it does have is plenty of electricity, and multiple ways to generate a lot more.

Let's concede that China's grid electricity, on which most of those EVs would be running, is among the highest in the world in emissions of both CO2 and local air pollutants. Switching China's new cars from gasoline and diesel to electricity won't constitute a big environmental win, initially or perhaps ever. Even under the relatively generous assumptions used in a recent analysis on Bloomberg, it will take the average EV in China 7 years to repay its extra lifecycle carbon debt, unless the country's electricity mix becomes much greener.

That seems realistic but almost beside the point, if China's main aim is to shore up its worsening energy security. Nor should we ignore the industrial-policy angle in such a move. China set out to dominate the global solar equipment market and can claim success, at least based on sales. If EVs catch on as many expect, the ultimate global market for them would be a sizable multiple of last year's $116 billion figure for global solar investment, only part of which relates to solar cell and module manufacturing, where China leads.

So let's assume 100% EVs is a given in China from some point in the next two decades. Does that spell the end of global oil demand growth in roughly the same timeframe? A number of recent forecasts, including those from Shell and Statoil, reached that conclusion even before the news about China's future car market.

It's not hard to envision this point of view solidifying into conventional wisdom, with interesting implications. Among other things, it could result in further cuts to investment in oil exploration and production that various experts including the International Energy Agency already worry could lead to another big oil price spike--well before EVs take off in a big way. It could also reduce R&D and investment in improvements to the conventional cars that will account for the large majority of car fleets and new car sales for some time to come, with adverse consequences for emissions.

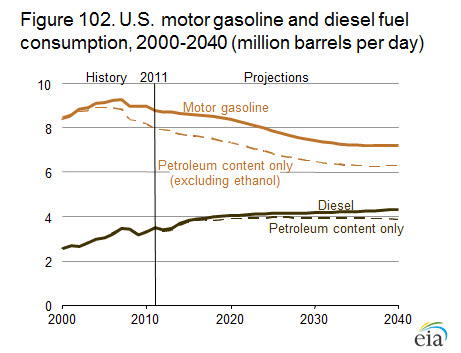

When I consider these forecasts I'm struck by how early we are in this particular transition. Global EV sales are still only around 1% of global car sales, and petroleum products account for all but a small sliver of the global transportation energy market. As fellow energy blogger Robert Rapier recently noted on Forbes, "China is a long way from reining in its oil consumption growth."

An excellent article by John Kemp in Reuters last week placed the shift away from coal in the context of a long sequence of historical energy transitions. As he noted, "Each step in the grand energy transition has seen the dominant fuel replaced by one that is more convenient and useful." Although there are other, compelling rationales for a move in the direction of electric vehicles backed by wind and solar power, it is extremely difficult to see that combination today in the terms Mr. Kemp used.

Pairing EVs with vehicle autonomy might create a product that is indeed more convenient and useful than current ICE cars with their effectively unlimited range and short refueling times. Perhaps it will require packaging self-driving EVs into mobility-on-demand services to beat that standard. It remains to be seen whether such a package would be technically or commercially viable, since even Tesla's "Autopilot" feature is still a far cry from such level 4 or 5 autonomy.

And even if EVs win the battle for car consumers with sustained help from governments, electricity is still an energy carrier, not an energy source. Renewables may go a long way toward replacing coal in the next two decades, but dispensing with both coal's 28% contribution to global primary energy consumption and oil's 33% in such a short interval looks like a massive stretch. Before the transition to EVs is complete, we may see at least some of them running on electricity generated by gas turbines burning petroleum distillates such as kerosene. (The environmental impacts of such a linkage would be significantly lower than running a fleet of EVs on coal.)

So while China's likely ban on internal combustion engine cars certainly looks like a key step on the path to peak oil demand, it could just as easily force oil producers to find new markets. That happened over a century ago, when a much smaller oil industry saw kerosene lose out to electric lighting and was farsighted or lucky enough to shift its focus to fueling Mr. Ford's new automobiles.

Peak demand for oil definitely lies somewhere in our future, regardless of China's future vehicle choices. However, as a long-time practitioner of scenario planning, my faith in precise forecasts extrapolated from current facts and trends is limited. Whether we are close to peak demand or, as with a global peak in oil supply, continue to push it farther off, will remain subject to uncertainties that won't be resolved for some time. Our best indication of either peak--demand or supply--will come when we have passed it. However, the idea of an impending peak has shown great potential to affect markets and decisions in the meantime.

{kind=link}